Florida Irrevocable Trust Planning: Building Durable Estate Strategies

An irrevocable trust is one of the most powerful tools available to Florida residents who want to protect assets and reduce taxes. Once you sign the documents, you cannot change or cancel the trust, which is exactly what makes it so effective for estate planning.

At Rubino Findley, PLLC, we help families in Palm Beach County understand how Florida irrevocable trust planning works and which strategies fit their specific situation. The right trust structure can shield your wealth from creditors, lower your tax burden, and ensure your assets pass to your heirs exactly as you intend.

What an Irrevocable Trust Actually Is and How It Works in Boca Raton

The Core Structure and Legal Framework

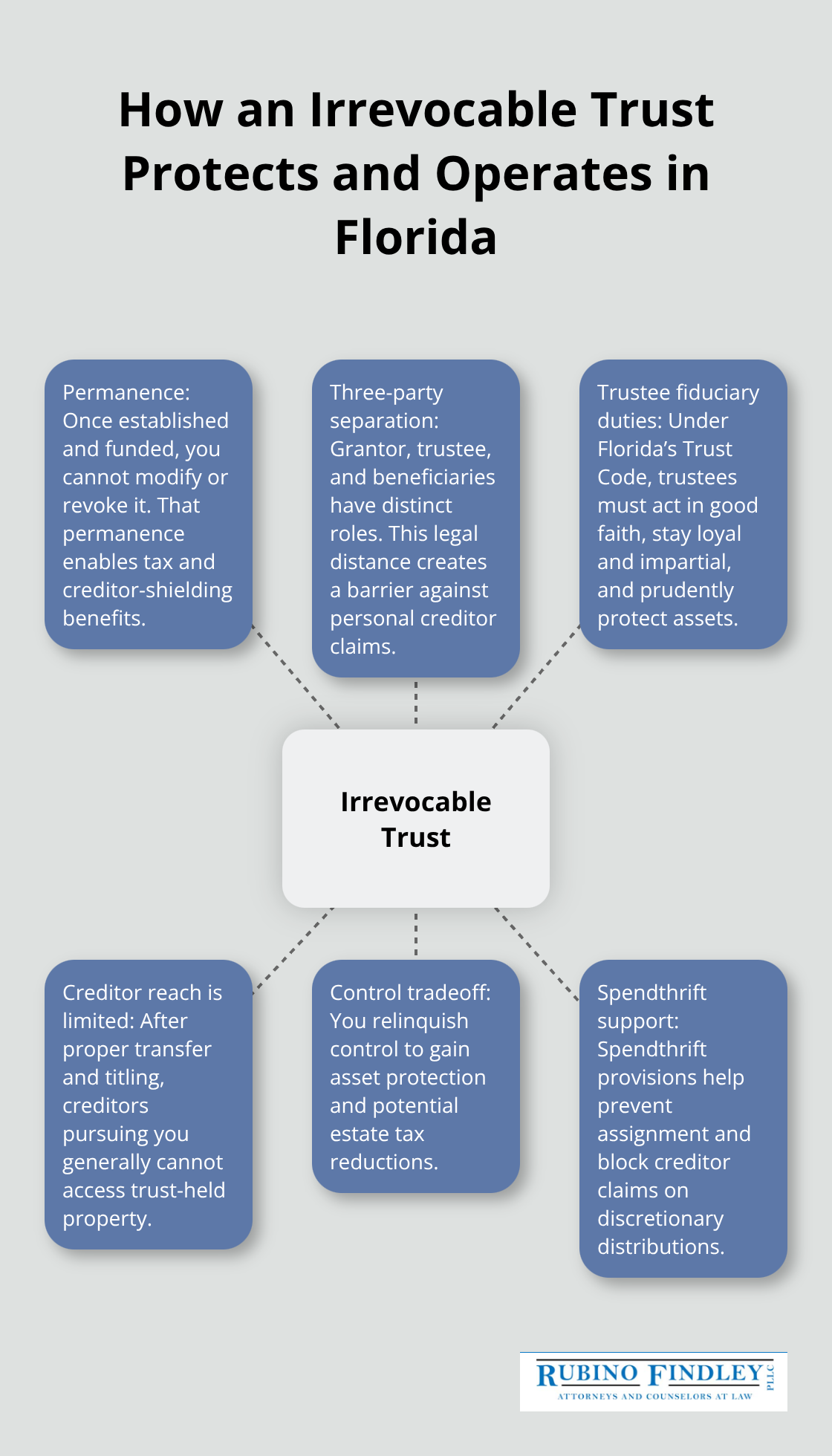

An irrevocable trust in Florida is a legal arrangement where you permanently transfer assets to a trustee who holds and manages them for your beneficiaries. According to the Florida Bar, trusts created in Florida after July 1, 2007 are revocable unless the document explicitly states irrevocable, which means you must be intentional about creating one. Once established and funded, an irrevocable trust cannot be modified, amended, or revoked-this permanence is not a limitation but rather the source of its power. The three-party structure separates you as the grantor, the trustee as the asset holder, and your beneficiaries as the recipients, creating legal distance that shields assets from creditors and judgment claims. Florida law (Chapter 736, the Florida Trust Code) governs how trustees must act, requiring them to administer the trust in good faith, remain loyal to beneficiaries, act impartially, and protect trust property with prudence.

The American Bar Association notes that this separation of ownership strengthens asset protection because creditors cannot reach assets held in the trust’s name once the transfer is complete.

Control Versus Protection: The Irrevocable Difference

The critical difference between irrevocable and revocable trusts is control versus protection. A revocable trust lets you retain complete control-you can change beneficiaries, modify terms, or dissolve the trust at any time-but assets remain in your taxable estate, offering no creditor protection or estate tax reduction. An irrevocable trust strips you of control permanently, but it removes assets from your taxable estate, shields them from creditors, and can reduce federal estate taxes substantially. The Internal Revenue Service allows you to use annual gift tax exclusions (currently $19,000 per beneficiary in 2025) when funding an irrevocable trust, minimizing or eliminating gift tax exposure.

Florida’s Unique Rules and Execution Requirements

Florida does not recognize self-settled domestic asset protection trusts for your own benefit, but you can create irrevocable trusts that benefit others or use specialized structures like spousal limited access trusts (SLATs) that preserve access for a non-settlor spouse while providing creditor protection. Execution in Florida requires two witnesses and a notary, and a self-proving affidavit simplifies future court proceedings. The decision hinges on your priorities: if you want flexibility and control, a revocable trust is appropriate; if you prioritize asset protection, tax reduction, and Medicaid planning, an irrevocable trust delivers those benefits at the cost of permanent relinquishment of control. Understanding which structure aligns with your family’s needs sets the foundation for the specific trust strategies that work best for Palm Beach County residents.

Why Irrevocable Trusts Cut Your Taxes and Shield Assets in Boca Raton

Estate Tax Reduction Through Asset Removal

Irrevocable trusts deliver two financial outcomes that revocable trusts cannot: they remove assets from your taxable estate and create a legal barrier between your wealth and creditors. The Internal Revenue Service allows you to transfer assets into an irrevocable trust using your annual gift tax exclusion, which is $19,000 per beneficiary in 2025. For married couples, that means $38,000 per beneficiary per year can move into the trust without triggering gift tax or consuming your lifetime exemption of $13.61 million. Over a decade, a married couple can transfer nearly $3.8 million to an irrevocable trust for a single beneficiary while avoiding gift tax entirely. The moment those assets leave your name and enter the trust, they stop growing your taxable estate. According to the Internal Revenue Service, this removal from your estate can reduce federal estate taxes substantially when you pass away, especially if your assets appreciate significantly while held in the trust.

Creditor Protection and Liability Shielding

Creditor protection works differently with irrevocable trusts because you no longer own the assets legally. Once the trustee holds title, creditors pursuing you cannot reach trust property, even if you face a lawsuit for malpractice, a car accident, or a business judgment. Florida law strengthens this protection through spendthrift provisions, which prevent beneficiaries from assigning their distributions to creditors and block creditor claims against discretionary distributions. The American Bar Association notes that this charging-order protection proves especially valuable for professionals in high-liability fields. The three-party structure (grantor, trustee, and beneficiary) creates legal distance that shields business assets from judgment claims once the transfer is complete.

Medicaid Planning and Long-Term Care Asset Protection

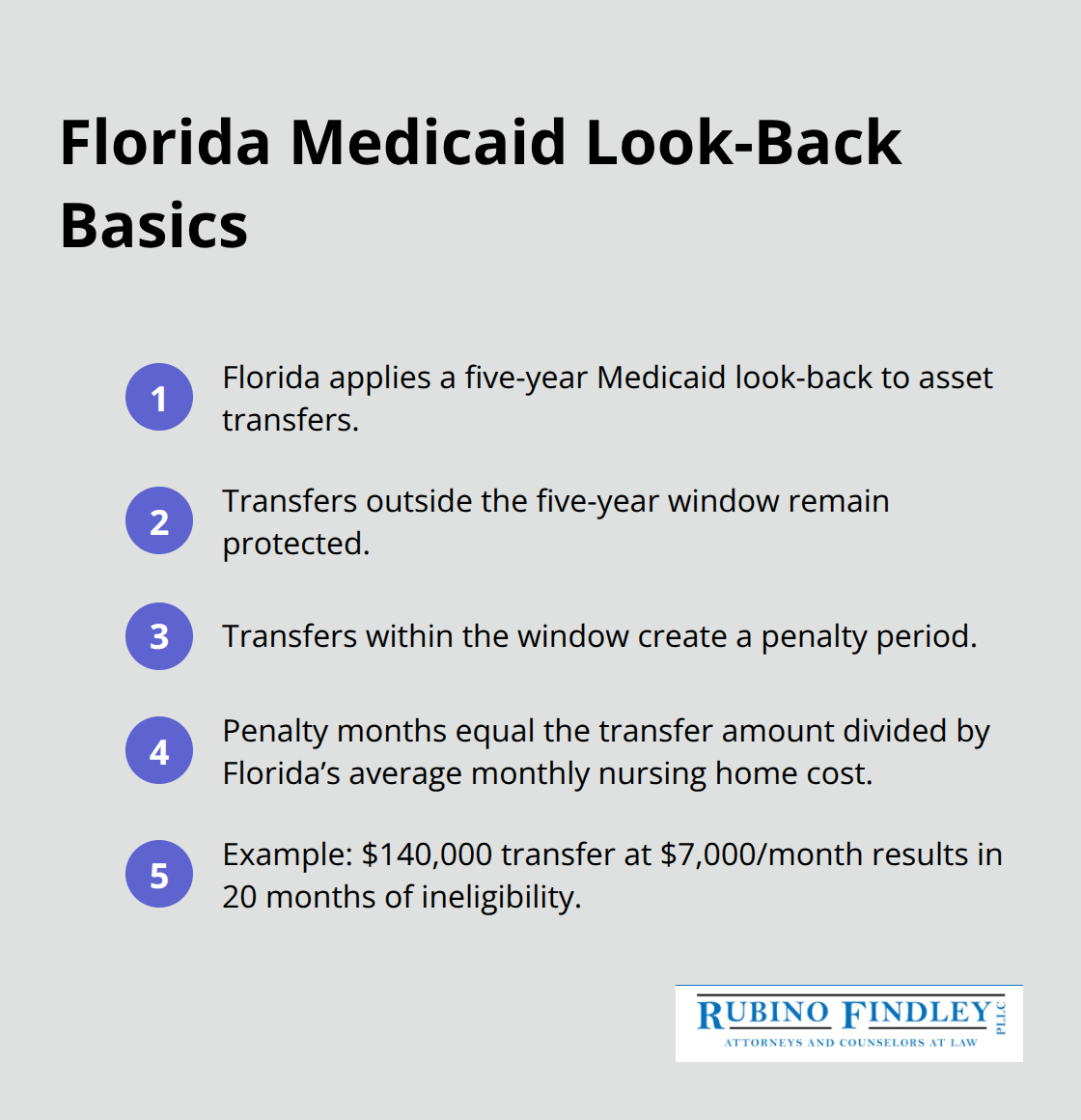

Medicaid planning represents a third advantage: if you face long-term care costs, an irrevocable trust funded at least five years before you apply for Medicaid can shelter assets from the program’s spend-down requirements. The five-year look-back, established by the National Academy of Elder Law Attorneys, evaluates all transfers in the five years before application. Assets transferred outside that window remain protected, while those within it trigger a penalty calculated by dividing the transfer amount by Florida’s average monthly nursing home cost. For someone facing $7,000 monthly care costs, a $140,000 transfer within five years creates a 20-month ineligibility period, but a transfer made six years earlier shelters that money entirely.

Planning ahead with an irrevocable trust preserves wealth for your heirs instead of spending it on institutional care.

These financial advantages make irrevocable trusts powerful tools, but they require careful structuring to align with your specific goals. The next section explores the most effective irrevocable trust strategies that Palm Beach County residents use to maximize these benefits.

Three Irrevocable Trust Strategies That Work in Boca Raton

Charitable Remainder Trusts for Philanthropic Goals

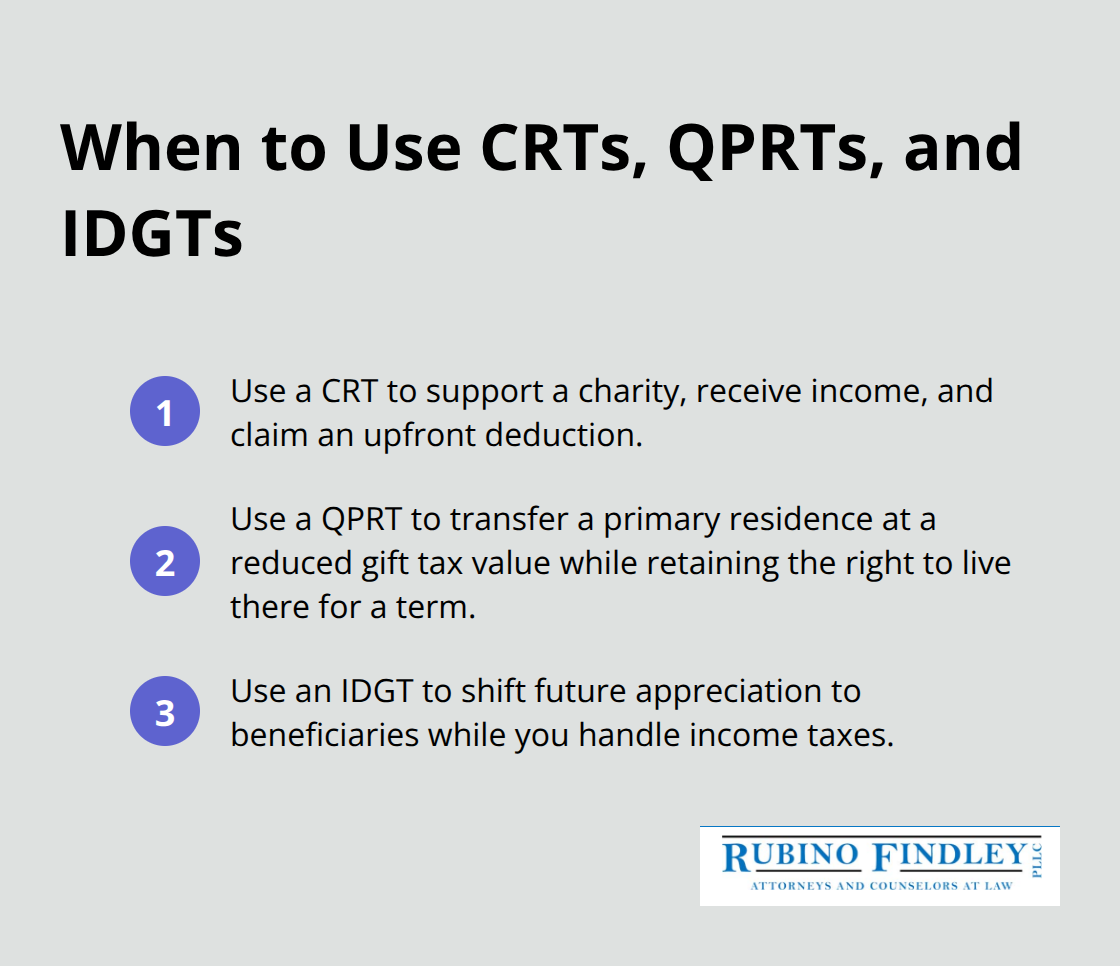

A Charitable Remainder Trust (CRT) transfers appreciated assets like real estate or securities to a trust while you receive an income stream for life or a set number of years, with the remainder passing to a qualified charity at the end. The immediate benefit is an upfront charitable tax deduction based on the present value of the remainder interest-for someone transferring a $500,000 portfolio at age 65 with a 6% annual payout, the IRS-prescribed valuation might yield a $150,000 to $200,000 deduction depending on your life expectancy and the payout rate. The Internal Revenue Service allows this deduction in the year the CRT is funded, which can offset income in that year or carry forward to reduce taxes in future years. You continue receiving distributions from the trust’s income and principal, so you maintain access to your wealth-you simply redirect it while supporting a cause you care about. The trust avoids probate, and the appreciated assets inside avoid capital gains tax when transferred into the CRT, meaning the trustee can sell the $500,000 portfolio without triggering $100,000 in capital gains tax that you would owe if you sold it personally. This strategy works best for donors with substantial appreciated assets, strong charitable intentions, and a desire to reduce taxes while maintaining retirement income.

Qualified Personal Residence Trusts for Home Transfers

A Qualified Personal Residence Trust (QPRT) transfers your home to beneficiaries at a dramatically reduced gift tax cost while you retain the right to live in the home rent-free for a specified period, typically 10 to 15 years. If your Boca Raton home is worth $1 million and you establish a 15-year QPRT, the gift tax value drops to perhaps $400,000 to $500,000 depending on IRS interest rates, meaning you use only that reduced amount against your lifetime gift tax exemption instead of the full $1 million. During the trust term, you retain full use and possession of the home, pay property taxes and insurance, and maintain all the benefits of ownership-the only change is that the legal title sits in the trust’s name. When the term ends, the home belongs to your beneficiaries free of additional gift or estate tax, and if you want to remain in the home, you can pay fair market rent to the trust, which becomes an asset your beneficiaries inherit. The strategy works because the IRS values the gift at a discount reflecting the fact that you retain use for the specified period.

Intentional Defective Grantor Trusts for Wealth Acceleration

An Intentional Defective Grantor Trust (IDGT) is structured so that you are treated as the owner for income tax purposes but the trust is treated as a separate entity for estate and gift tax purposes, creating a powerful wealth-transfer mechanism. You fund the IDGT with assets expected to appreciate substantially-perhaps a growing business interest, real estate, or a portfolio of growth stocks-and you sell those assets to the trust in exchange for a promissory note at an IRS-prescribed interest rate, currently around 5% to 6%. The trust makes payments on the note, but because you are the grantor for income tax purposes, you pay the income tax on the trust’s earnings while the trust’s principal grows untaxed. Over time, the assets inside the IDGT appreciate well beyond the interest rate you charge, and that appreciation transfers to your beneficiaries without consuming additional gift tax exemption. If the assets grow from $1 million to $3 million over 10 years, the $2 million gain transfers to your beneficiaries estate-tax-free because the growth occurred inside the trust after the initial funding.

Matching Strategies to Your Financial Goals

CRTs work for philanthropic donors seeking income and tax deductions, QPRTs work for homeowners wanting to transfer primary residences at reduced tax cost, and IDGTs work for those holding appreciating assets and wanting to shift future growth to beneficiaries without gift tax consequences. Each strategy addresses different objectives and requires careful structuring to align with your specific situation and family priorities.

Final Thoughts on Florida Irrevocable Trust Planning in Boca Raton

Florida irrevocable trust planning requires precision in how you word the irrevocability clause, structure distributions, and fund the trust. The Florida Trust Code (Chapter 736) sets strict requirements for trustee duties, beneficiary notifications, and trust administration that differ from other states, and a single mistake can undermine your entire strategy. If you fail to explicitly declare a trust irrevocable in the document, Florida law treats it as revocable by default, which eliminates the asset protection and tax benefits you intended. Improper funding-transferring assets into the trust name without updating deeds, retitling accounts, or changing beneficiary designations-leaves those assets outside the trust entirely and exposes them to creditors and probate.

The strategies discussed here (Charitable Remainder Trusts, Qualified Personal Residence Trusts, and Intentional Defective Grantor Trusts) each carry specific IRS requirements, valuation rules, and ongoing compliance obligations that demand careful attention. A CRT must distribute income annually; a QPRT requires you to survive the term to achieve the tax benefit; an IDGT demands careful note documentation and interest payments. Missing these requirements triggers unexpected tax bills or causes the IRS to recharacterize the trust entirely, so you cannot treat these structures as set-and-forget arrangements.

Your trust must align with your family’s actual goals and financial situation, not a generic template that cannot account for your specific assets, beneficiaries, risk tolerance, or long-term vision. We at Rubino Findley, PLLC help families in Palm Beach County structure irrevocable trusts that match their priorities while complying with Florida law. Schedule your free consultation to discuss which trust strategy fits your situation.