High Net Worth Florida Estate Planning: Strategies For Luxurious Legacies

High net worth Florida residents face unique challenges when protecting their wealth across multiple generations. A generic will or basic trust simply won’t cut it when you have significant assets, business interests, and complex tax situations.

At Rubino Findley, PLLC, we’ve seen how the right planning strategies can save families hundreds of thousands in taxes while preserving their legacy exactly as intended. This guide walks you through the advanced approaches that actually work for substantial estates in Boca Raton and throughout Florida.

What Makes Florida’s Tax Environment Different for High Net Worth Planning

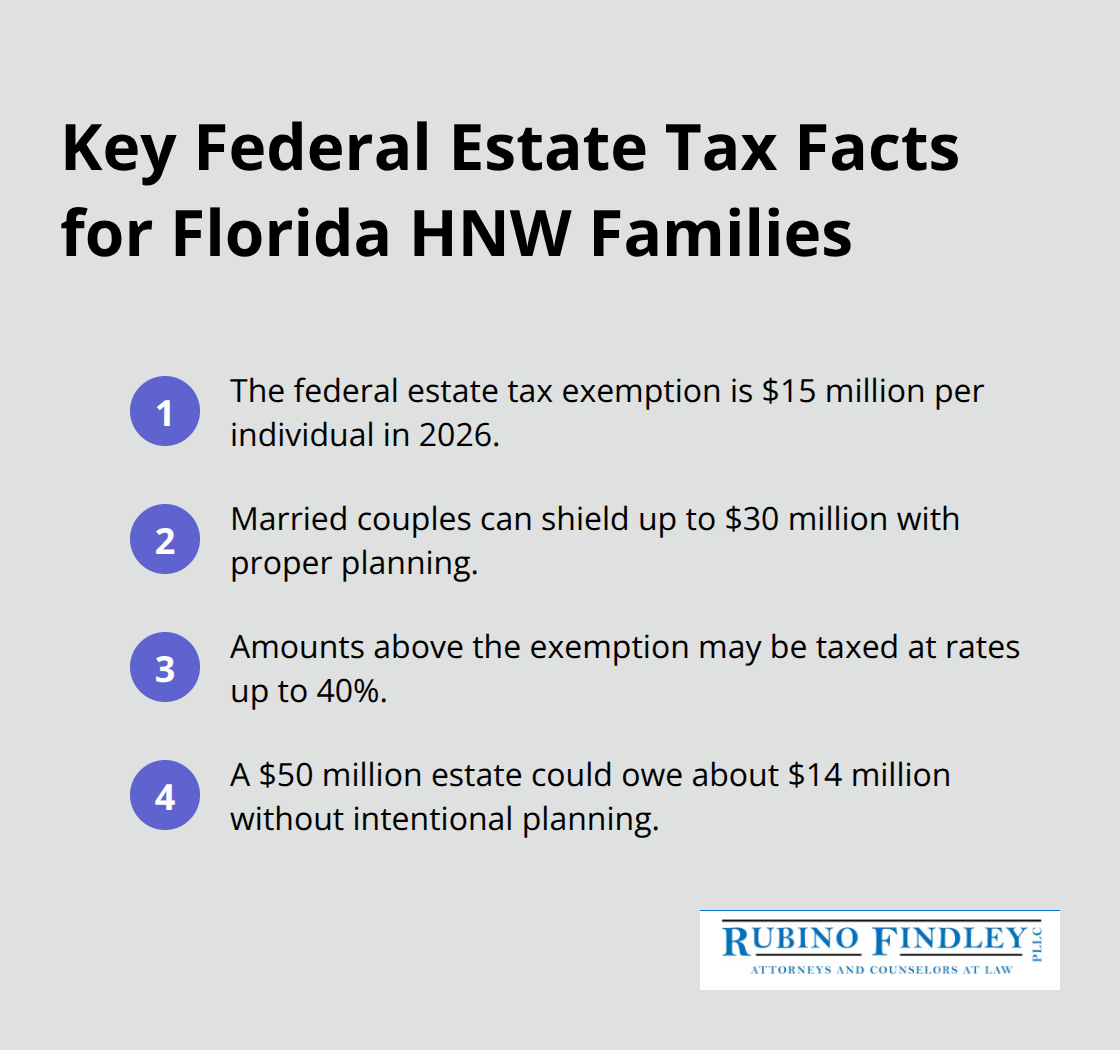

Florida’s lack of state estate and income taxes creates a significant financial advantage, but this benefit only materializes when you structure your assets strategically. The federal estate tax exemption stands at $15 million per individual in 2026, allowing married couples to shield up to $30 million in combined assets with proper planning. Wealth above this threshold faces federal taxation at up to 40%-a $50 million estate could owe $14 million in federal taxes without intentional planning. Many high net worth Floridians make their first critical mistake here: they assume no state tax means minimal tax exposure overall. The reality is far different. Your real estate holdings, investment portfolios, business interests, and retirement accounts all flow into your taxable estate at death, and federal rates hit hard once you cross the exemption threshold.

Real Assets Demand Real Planning Strategies

High net worth individuals in Palm Beach County typically hold assets that generic wills cannot address effectively. Waterfront properties in Jupiter appreciate consistently, making them core components of estate portfolios, but they also carry specific valuation challenges and probate complexities. Business interests present another layer of difficulty-if you own a company, a basic will offers no succession roadmap, leaving employees, partners, and heirs in chaos. Retirement accounts with millions in accumulated value, investment portfolios with significant unrealized gains, and luxury items all require explicit planning to minimize taxes and transfer smoothly. A standard will treats these assets the same way, which wastes opportunities to use trusts, gifting strategies, and ownership structures that could reduce your taxable estate. When assets flow through probate, your family also faces court costs, delays, and public disclosure of your financial situation. For substantial estates, probate becomes an expensive, lengthy process that you could have avoided entirely with a revocable living trust established years earlier.

Tax-Reduction Tools That Generic Plans Miss

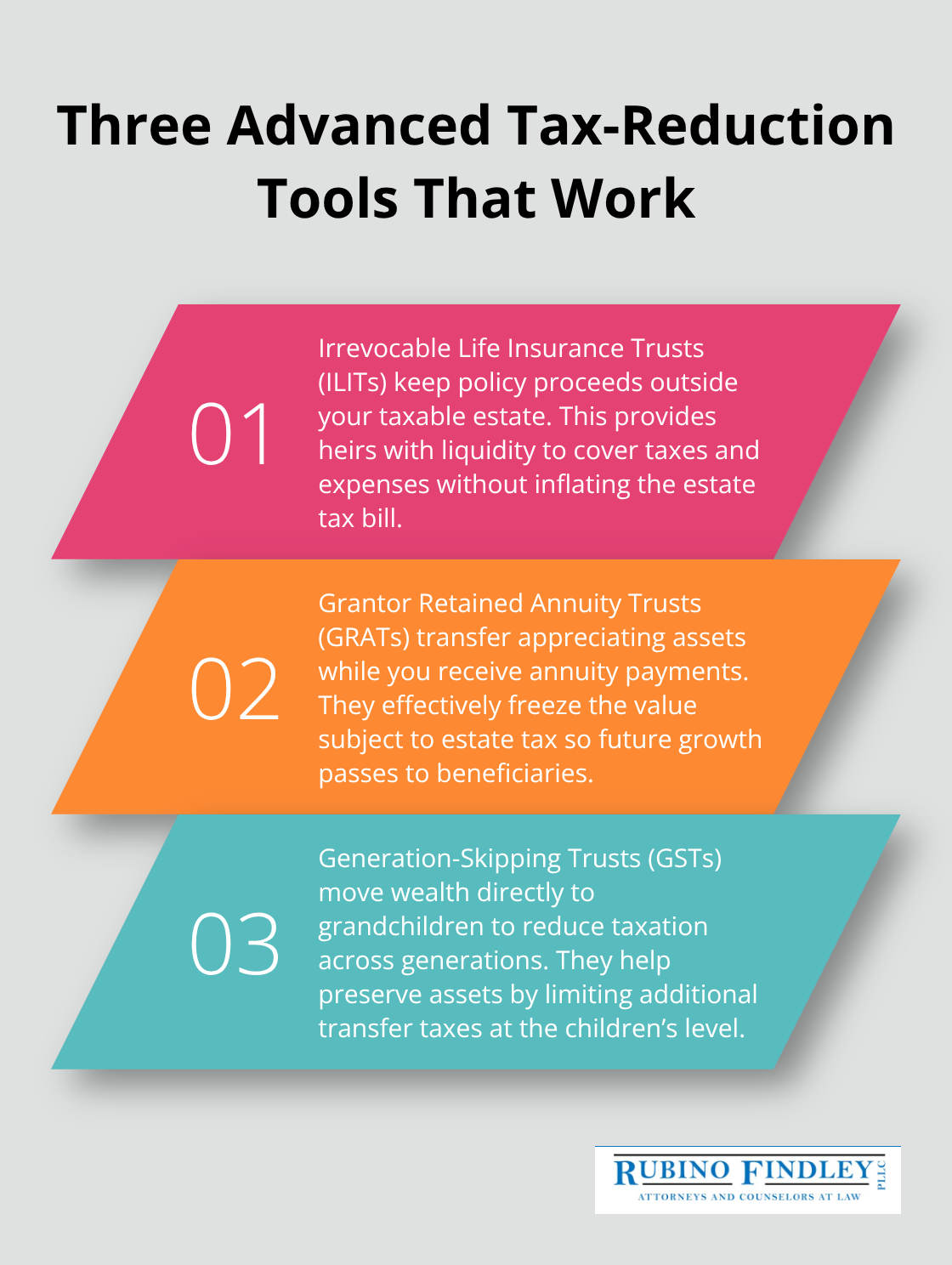

A one-size-fits-all estate plan ignores the tax-reduction tools available to you. Irrevocable Life Insurance Trusts hold life insurance proceeds outside your taxable estate, providing liquidity to heirs without increasing estate taxes. Grantor Retained Annuity Trusts allow you to transfer appreciating assets to beneficiaries while you receive annuity payments, effectively freezing the value subject to estate tax.

Generation-Skipping Trusts move wealth directly to grandchildren with reduced tax exposure across generations. These strategies require careful setup and ongoing management, but they work only if you implement them before death. Family Limited Partnerships and LLCs can hold real estate and business interests, allowing you to transfer ownership incrementally while you maintain control and manage distributions. The annual gift exclusion of $19,000 per recipient per year represents another powerful tool-couples can gift $38,000 annually to each child without triggering gift tax filings. Over a decade, a couple could move nearly $400,000 out of their taxable estate through systematic gifting, yet many high net worth individuals never implement this strategy because their estate plan never addressed it.

Moving Forward With Strategic Asset Protection

The gap between a basic will and a comprehensive estate strategy determines whether your family preserves wealth or watches it disappear to taxes and probate costs. Your next step involves identifying which of your assets require special attention and which tax-reduction strategies align with your family’s goals. This assessment forms the foundation for everything that follows in your estate plan.

How Trusts, Succession Plans, and Asset Protection Work Together in Boca Raton

Irrevocable Trusts Remove Assets From Your Taxable Estate

Irrevocable trusts form the backbone of wealth protection for high net worth families in Palm Beach County. When you place assets into an irrevocable trust, you remove them from your taxable estate permanently, which means they no longer count toward the $15 million federal exemption threshold. This distinction matters enormously: a $5 million waterfront property in Jupiter held in an irrevocable trust avoids the 40% federal estate tax that would otherwise apply, saving your heirs $2 million in taxes. Irrevocable Life Insurance Trusts specifically solve a common problem-life insurance proceeds normally flow into your taxable estate at death, but when held in an ILIT, they sit outside the estate entirely and provide liquidity to cover taxes without burdening heirs with asset sales.

Qualified Personal Residence Trusts let you transfer high-value Florida real estate to beneficiaries while retaining the right to live in the property during a set term, effectively freezing the asset’s value for tax purposes. The mechanics require careful drafting: you must transfer assets to the trust, retitle deeds and accounts properly, and avoid any actions that suggest you still control the assets. Many families hesitate because irrevocable means you cannot undo the transfer, but that permanent nature is precisely what creates the tax benefit. The trade-off proves worthwhile when your estate exceeds the exemption and every million dollars matters.

Business Succession Planning Protects Company Value and Employees

Business owners face a separate but equally urgent challenge-succession planning that protects employees, maintains company value, and minimizes taxes simultaneously. Without explicit succession documents, a family business can lose 30% to 50% of its value within two years of the owner’s death, according to research from the U.S. Small Business Administration. A buy-sell agreement funded with life insurance solves this directly: if you own a business with partners, the agreement specifies who purchases your shares at death and life insurance inside an ILIT provides the cash immediately, preventing forced asset sales or loss of control.

For sole proprietors, a clear succession plan names a successor, documents their training timeline, and establishes management authority to prevent the business from collapsing during transition. Family Limited Partnerships and LLCs serve dual purposes-they hold business interests or real estate while allowing you to transfer ownership incrementally to heirs without relinquishing control. You retain the general partner position, making decisions about distributions and operations, while heirs gradually own limited partnership interests that appreciate tax-efficiently over time.

Asset Protection Trusts Shield Wealth From Creditors and Claims

Asset protection trusts add another layer by shielding inherited assets from creditors, divorce claims, and lawsuits against beneficiaries. Spendthrift provisions inside these trusts prevent a beneficiary from selling inherited assets or pledging them as collateral, which protects vulnerable family members from poor financial decisions or predatory lending. Florida’s homestead exemption already protects your primary residence from most creditors, but investment properties, business interests, and liquid assets need these trust-based protections to remain secure across generations.

The combination of irrevocable trusts, succession planning structures, and asset protection mechanisms creates a comprehensive framework that addresses multiple threats simultaneously. Your business transfers smoothly to the next generation, your real estate and investments remain protected from external claims, and your taxable estate shrinks significantly through strategic asset removal. These tools work together because each one addresses a specific vulnerability in a high net worth portfolio. The next step involves identifying which specific structures fit your family’s situation and implementing them before circumstances force reactive decisions.

What Derails High Net Worth Estate Plans in Boca Raton

Outdated Plans Create Tax Disasters

High net worth families in Palm Beach County make three predictable but devastating mistakes that undermine otherwise solid estate plans. The first mistake happens silently over years: your plan becomes dangerously outdated after major life changes. You established a comprehensive trust structure when your net worth was $8 million, but your business sold for $25 million, or you inherited significant assets, or your family structure shifted through marriage or divorce. The plan that protected you then no longer serves your current situation. Federal estate tax exemptions also change regularly-the $15 million threshold in 2026 will drop to approximately $7 million per individual in 2027 unless Congress acts, which means strategies that worked last year may fail spectacularly next year. Clients who implemented a gifting strategy five years ago with a $12 million exemption now face a fundamentally different tax landscape. Your asset mix changes too. A portfolio weighted heavily toward appreciating real estate in Jupiter requires different tax strategies than one concentrated in liquid investments or business interests. Without regular reviews-ideally annually or whenever significant changes occur-your plan drifts further from reality with each passing year.

Underestimating Federal Tax Consequences

The second mistake involves fundamentally underestimating federal tax consequences. Many high net worth Floridians fixate on Florida’s lack of state estate tax and assume their tax exposure is minimal. This creates dangerous complacency. A $35 million estate with the 2026 exemption faces $8 million in federal taxes on the $20 million above the threshold, assuming no planning. Add a spouse with separate assets and the calculation becomes more complex but not necessarily better. The math shifts dramatically when you consider that wealth above the exemption threshold faces taxation at up to 40%. A $50 million estate could owe $14 million in federal taxes without intentional planning. This reality demands that high net worth individuals stop treating Florida’s tax advantages as a substitute for comprehensive federal tax strategy.

Neglecting Incapacity Planning Proves Equally Costly

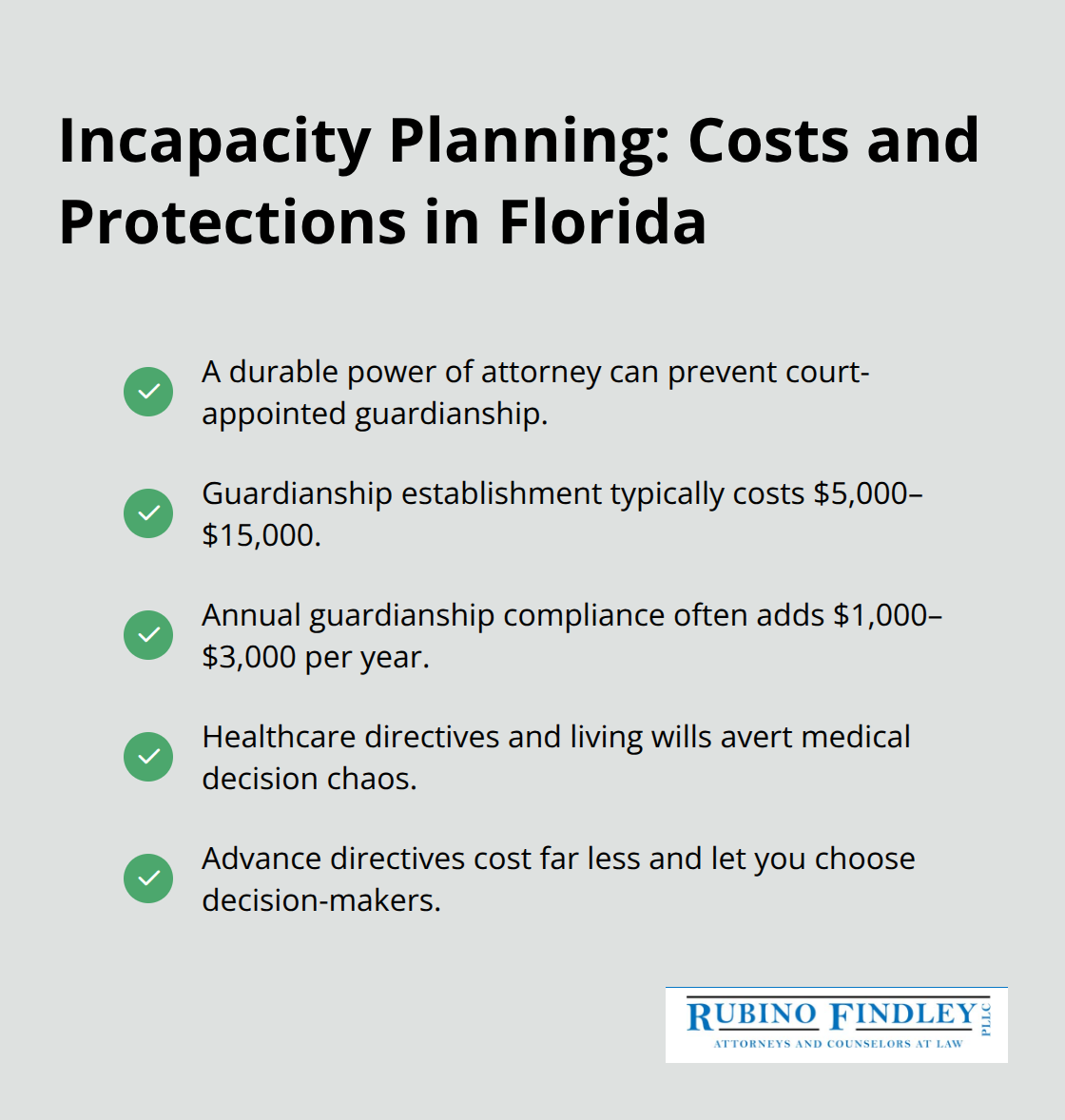

The third critical mistake is neglecting incapacity planning entirely, which proves equally expensive and disruptive as poor tax planning. You have an irrevocable trust protecting your assets and a sophisticated business succession plan in place, but you suffer a stroke at age 62 and cannot communicate your wishes for three years. Without a properly executed durable power of attorney naming someone you trust, Florida courts must appoint a guardian-a costly, public process that strips you of financial control and requires your designated guardian to post a bond and file annual accountings with the court. Healthcare directives and living wills prevent similar chaos in medical decisions. The costs of guardianship proceedings in Florida typically run $5,000 to $15,000 just to establish, then ongoing annual compliance costs of $1,000 to $3,000. An advance care directive and durable power of attorney cost a fraction of that amount and give you complete control over who makes decisions if you cannot.

The Path Forward Requires Discipline

These three categories of mistakes-stale plans, underestimated taxes, and ignored incapacity provisions-destroy more high net worth estates than any single planning failure. The solutions require discipline: schedule annual plan reviews, work with professionals who understand current exemption thresholds and tax law changes, and ensure your incapacity documents are as detailed and legally sound as your wealth transfer strategies. When you partner with an experienced estate planning attorney from Rubino Findley, PLLC in Boca Raton, you gain access to professionals who help clients throughout Palm Beach County avoid these costly errors through regular strategy reviews and comprehensive planning that addresses tax, incapacity, and asset protection simultaneously.

Final Thoughts on Building Your Legacy in Boca Raton

The strategies outlined throughout this guide only work when you implement them with professional guidance and maintain them over time. High net worth Florida residents cannot afford to treat estate planning as a one-time task completed years ago and then forgotten. Your plan must evolve as your circumstances change, tax laws shift, and your family’s needs develop.

Coordinating your estate strategy requires professionals who understand both the technical details and your personal goals. An experienced estate planning attorney works alongside your financial advisors, tax professionals, and insurance specialists to ensure every piece of your plan fits together seamlessly. At Rubino Findley, PLLC in Boca Raton, we help clients throughout Palm Beach County establish wills, trusts, durable powers of attorney, and comprehensive strategies that address tax efficiency, asset protection, and incapacity planning simultaneously. This coordination prevents gaps where assets fall through the cracks or where conflicting strategies undermine your overall objectives.

Schedule annual check-ins to assess whether major life changes, tax law modifications, or shifts in your asset mix require adjustments (a plan that protected you effectively at $10 million in net worth may create unintended consequences at $25 million). Written instructions about your charitable giving intentions, family values you want to pass forward, and specific wishes for business succession or property management provide clarity that prevents disputes among heirs. Contact Rubino Findley, PLLC to schedule your free consultation and begin building the comprehensive estate plan your family deserves.