Florida Business Estate Planning: Securing Your Company and Heirs

Most Florida business owners focus on growing their companies but overlook what happens when they’re gone. Without a solid plan, your life’s work could face legal battles, tax penalties, or even forced sales.

Florida business estate planning protects both your company and your family’s financial future. We at Rubino Findley, PLLC in Boca Raton help business owners create plans that address succession, taxes, and asset protection.

Why Business Estate Planning Matters for Florida Owners

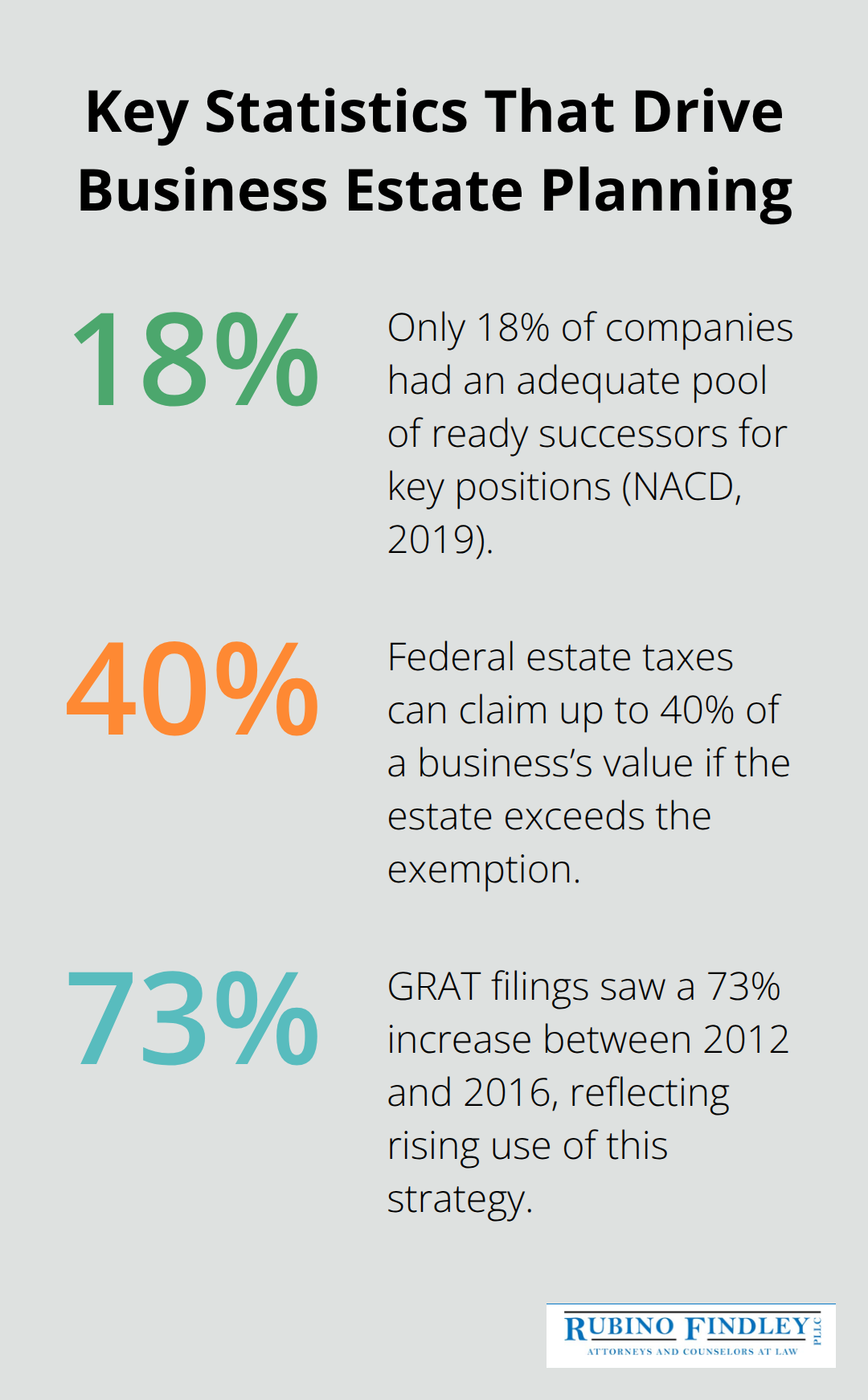

Probate costs money and time that your heirs won’t have. When a business owner dies without a plan, their company becomes part of the probate process, which in Florida can drag on for months or even years. Court fees, legal expenses, and administrative costs eat into the assets your family should inherit. A 2019 National Association of Corporate Directors survey found that only 18 percent of companies had an adequate pool of ready successors for key positions, meaning most businesses face immediate leadership gaps when an owner passes away.

Without succession documentation in place, your business loses clients, key employees leave, and revenue drops sharply during the transition.

Family Conflict Destroys Business Value

Family arguments over business assets destroy relationships and drain finances. When there’s no written succession plan, siblings or spouses often disagree about who should run the company, how to divide it, or whether to sell it. These conflicts lead to costly litigation that further depletes business value. A buy-sell agreement eliminates guesswork by clearly stating what happens if an owner dies, becomes disabled, or retires. Life insurance funds the buyout, so remaining owners have cash to purchase the departing owner’s stake without draining operating capital. This approach keeps the business running smoothly and prevents family members from fighting in court.

Federal Taxes Can Claim Half Your Legacy

Federal estate taxes can claim up to 40 percent of your business value if your estate exceeds the exemption threshold. As of 2023, the federal exemption was $12.92 million per individual, but Congress has not acted to prevent that exemption from dropping significantly in 2026. Florida has no state estate tax, which is advantageous, but federal taxes still apply to your business interests. Strategic tools like Family Limited Partnerships create valuation discounts of up to 40 percent according to a 2021 American Bar Association study, allowing you to transfer more wealth to heirs with minimal gift tax consequences. Grantor Retained Annuity Trusts offer another path to move appreciating assets forward, with IRS data showing a 73 percent increase in GRAT filings between 2012 and 2016. Irrevocable Life Insurance Trusts keep insurance proceeds outside your taxable estate, preserving liquidity for your business and family. The annual gift tax exclusion-$17,000 per recipient as of 2023-lets you transfer wealth gradually without triggering gift taxes. Starting these strategies now gives your heirs substantially more of what you built.

What Comes Next

The right business structure and succession documents form the foundation of protection. Understanding which tools fit your situation requires a closer look at the specific components that make a plan work.

Building the Right Foundation for Your Business Succession

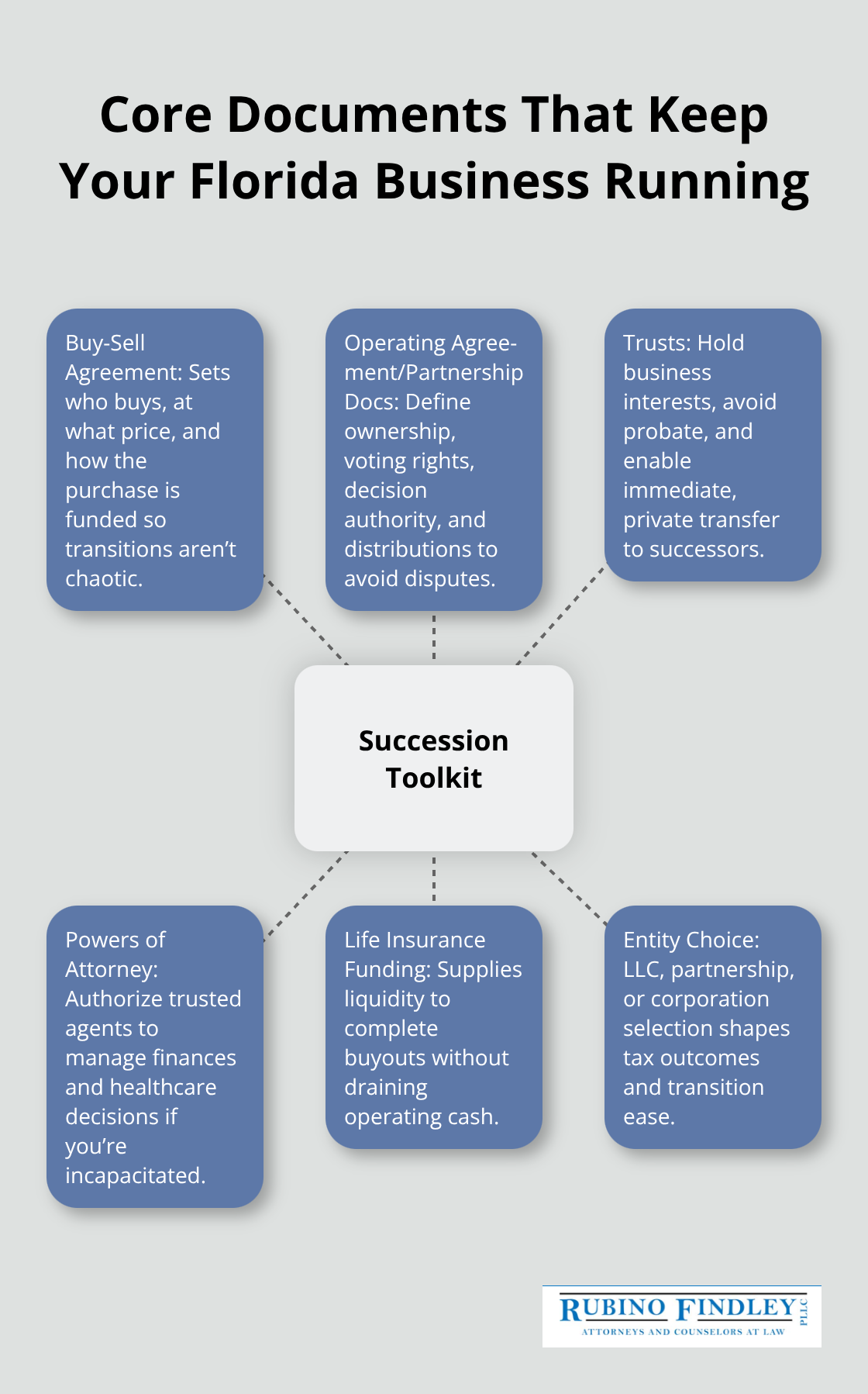

A buy-sell agreement stands as the single most important document you can create as a business owner. This agreement specifies exactly what happens when an owner dies, becomes disabled, or retires-no guesswork, no family arguments, no forced sales at fire-sale prices. The agreement names a successor, sets the purchase price, and defines how the transaction receives funding. Without it, your heirs inherit a business they may not want to run, and co-owners face uncertainty about whether they can afford to buy out the departing owner’s stake.

Life insurance funds these buyouts directly, so the cash appears automatically when needed. A properly structured buy-sell agreement prevents your family from liquidating the company in a panic or watching it deteriorate while your estate sits in probate.

Operating Agreements Establish Clear Rules

You should establish clear operating agreements or partnership documents that outline ownership percentages, voting rights, and distribution rules before any transition occurs. These documents become your roadmap during uncertainty and protect all parties involved. They specify how decisions get made, who holds authority over what, and how profits flow to owners. Without these agreements in place, state law determines the outcome-and state law rarely aligns with what you actually want for your business.

Trusts Shield Assets and Control

A revocable living trust holds your business interest and operates during your lifetime, then transfers smoothly to your chosen successor when you die or become incapacitated. The trustee named in your trust takes over immediately without court involvement, so operations continue without interruption. Unlike a will, a trust avoids probate entirely and keeps your business details private-no court filings, no public record of what you owned or who inherited it.

Family Limited Partnerships create significant valuation discounts that reduce gift and estate taxes; the American Bar Association documented discounts of up to 40 percent when structured correctly. Irrevocable Life Insurance Trusts own your business insurance policies outside your taxable estate, preserving the full death benefit for your heirs rather than losing it to federal taxes. These trusts require careful setup with proper compliance, so professional guidance matters.

Powers of Attorney Protect Your Interests

A durable power of attorney names someone you trust to manage your business finances and decisions if you become unable to act yourself. Healthcare directives specify who makes medical decisions on your behalf, preventing family conflict and ensuring your stated wishes guide treatment. Without these documents in place, a court may appoint a guardian or conservator to manage your affairs, costing thousands in legal fees and removing your say from the process.

The specific structure you choose-whether an LLC, partnership, or corporation-affects how smoothly your succession plan works and what tax benefits you can access. Understanding which entity type aligns with your goals requires examining the practical differences between these options.

What Derails Business Estate Plans in Boca Raton

Most Florida business owners create an estate plan and then file it away, assuming the work is done. This approach guarantees failure. A business plan drafted five years ago no longer reflects your current ownership structure, tax laws, or family circumstances. The federal estate tax exemption of $12.92 million in 2023 is set to drop substantially in 2026 unless Congress acts, which means strategies that worked last year may leave your heirs facing unexpected tax bills. Without regular updates, your plan becomes outdated the moment circumstances change. Many owners also skip the succession documentation entirely, believing their heirs will understand what to do or that a handshake agreement with a co-owner is sufficient. When death or disability strikes, that missing paperwork creates immediate chaos. Co-owners discover they cannot afford to buy out the departing owner’s stake, clients question who is actually in charge, and key employees start looking for jobs elsewhere. The business deteriorates rapidly while your estate sits in probate, sometimes for over a year.

The Succession Documentation Gap

A buy-sell agreement with funded life insurance solves the biggest problem most owners ignore. Without it, your heirs inherit a business they may not understand or want to operate, and remaining co-owners face a financial crisis if they must purchase the departing stake. The agreement specifies exactly who buys the interest, at what price, and how the transaction receives funding. Life insurance provides the cash automatically, eliminating the need for loans or forced asset sales. Many owners also fail to create operating agreements that clearly define voting rights, profit distributions, and decision-making authority. When an owner dies or becomes incapacitated, state law fills the void, and state law rarely matches your actual intentions. Your heirs end up operating under rules you never chose, often creating disputes among family members. A properly documented operating agreement prevents this by establishing clear rules before any transition occurs. Additionally, owners frequently overlook the need for succession plans that identify specific successors, outline their responsibilities, and detail a transition timeline. Naming a successor in your will is not enough; you must prepare that person to lead the company and communicate the plan to key employees and clients well in advance.

Tax Strategy Blindness and Timing Delays

Owners who wait until they are older or facing health issues discover that valuable tax strategies are no longer available. Grantor Retained Annuity Trusts require time to work effectively, as the IRS data showed a 73 percent increase in GRAT filings between 2012 and 2016 among owners who understood their power. Family Limited Partnerships, which can create valuation discounts of up to 40 percent according to a 2021 American Bar Association study, need years to function properly and demonstrate legitimate business purpose before an estate tax audit. Starting these strategies now, rather than waiting until retirement, allows your heirs to receive substantially more of what you built. The annual gift tax exclusion of $17,000 per recipient as of 2023 lets you transfer wealth gradually without triggering gift taxes, but this only works if you start before a health crisis forces your hand. Owners also frequently overlook how their entity choice affects tax outcomes. An LLC, partnership, S corporation, or C corporation each creates different tax consequences for your heirs, and changing the structure later becomes complicated and expensive. Making the right choice at formation saves thousands in taxes and legal fees down the road.

Outdated Plans and Changing Circumstances

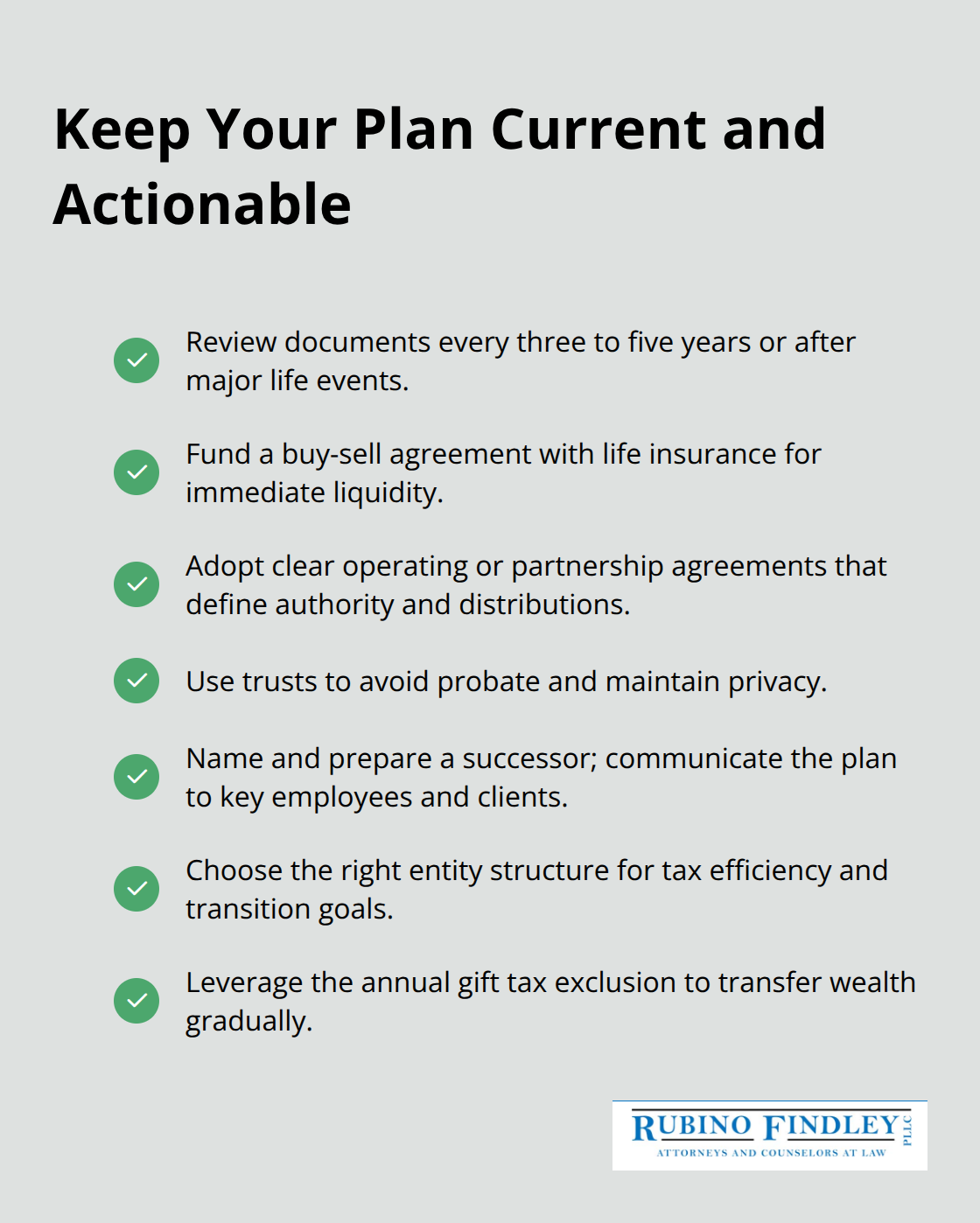

Your business grows, your family situation shifts, and tax laws change constantly. A plan that addressed your needs three years ago may create problems today. If you added a new partner, expanded into another state, or experienced a significant increase in business value, your existing documents no longer protect you adequately. Tax law changes happen frequently, and what was optimal in 2020 may cost you thousands in unnecessary taxes in 2026. Your family circumstances matter too-a divorce, remarriage, birth of children or grandchildren, or a child’s financial struggles all affect how your plan should work. Without regular reviews (ideally every three to five years or after major life events), your plan drifts further from your actual situation. Many owners also fail to communicate their plans to the people who will execute them. Your executor, trustee, or successor may not know where documents are stored, what your wishes actually are, or how to access business accounts and records.

This lack of communication transforms a well-drafted plan into a useless document that creates confusion rather than clarity when you need it most.

Final Thoughts

A solid Florida business estate planning strategy protects what you’ve built and ensures your family inherits what you intended, not what state law dictates. The core elements are straightforward: a buy-sell agreement funded by life insurance, clear operating documents, trusts that avoid probate, and powers of attorney that cover both financial and healthcare decisions. These tools work together to prevent family conflict, eliminate tax waste, and keep your business running smoothly during transitions.

Start by identifying your immediate priorities-do you have a successor in mind, or do you need to develop one? Is your current entity structure optimized for tax efficiency, or could a different approach save your heirs thousands? Have you funded a buy-sell agreement, or would your family face a financial crisis if you died tomorrow? These questions reveal where your plan has gaps and what needs attention first.

We at Rubino Findley, PLLC in Boca Raton help business owners throughout Palm Beach County create comprehensive plans that address succession, taxes, and asset protection. Contact us today to schedule your consultation and begin protecting your company and family legacy.