Florida Estate Taxes Overview: What Every Planner Should Know

Florida has no state estate tax, but federal rules still apply to residents in Palm Beach County and throughout the state. Understanding this Florida estate taxes overview is the first step toward protecting your family’s wealth.

At Rubino Findley, PLLC, we help residents navigate these rules and avoid costly mistakes. This guide covers the strategies that actually work.

What’s the Real Estate Tax Impact for Florida Residents in Boca Raton

Florida’s lack of state estate tax is a genuine advantage, but it creates a false sense of security for many residents in Palm Beach County. The federal government still taxes large estates at 40 percent above the exemption threshold, and that threshold is shrinking. Starting January 1, 2026, the federal exemption drops to approximately $15 million per person, down from the current $13.61 million.

For married couples, that means a combined exemption of roughly $30 million before the 40 percent tax kicks in. According to the IRS, fewer than 0.1 percent of estates nationwide owe federal estate tax, but that statistic hides a critical reality: high-net-worth Florida residents are increasingly falling into that small group as exemptions decline. If your estate will exceed these thresholds, federal taxes will consume significant wealth unless you act now.

The Exemption Cliff Arrives Soon

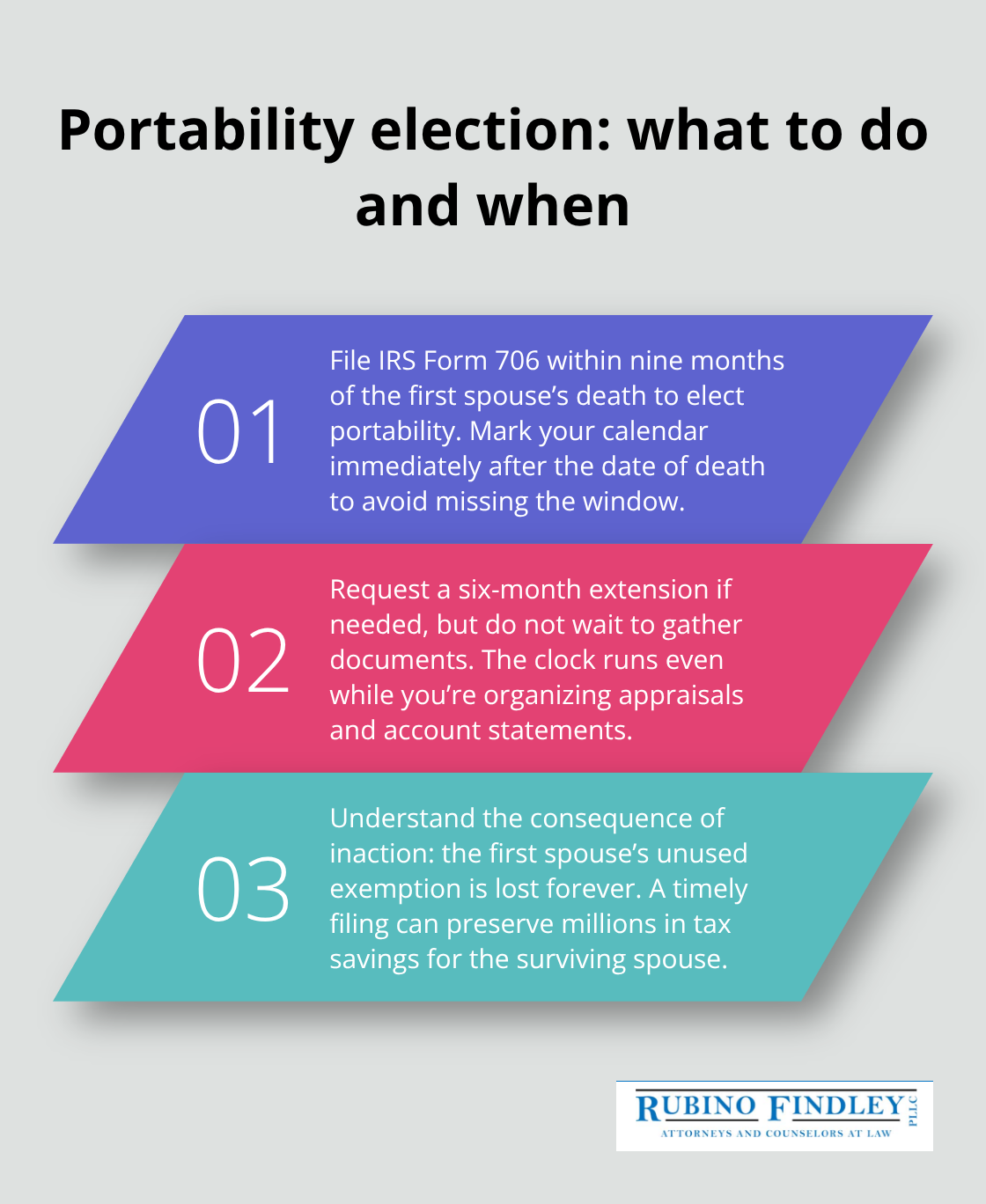

The federal exemption is scheduled to drop again in 2026 and will continue declining unless Congress acts. This means families with $12 million in assets today might face federal estate taxes in just a few years. The exemption applies to all assets, including real estate, investment accounts, retirement plans, and business interests. Married couples can use portability, which allows the surviving spouse to claim the deceased spouse’s unused exemption by filing IRS Form 706 within nine months (plus a six-month extension), but this requires deliberate action and proper documentation. Without filing the election, that exemption is lost forever. For Florida residents with significant wealth, waiting to see what happens with future exemptions is a risky strategy that could cost hundreds of thousands of dollars.

How the Stepped-Up Basis Works in Your Favor

The stepped-up basis rule under IRC Section 1014 is one of the most valuable tax benefits available to heirs, and it applies to all inherited assets in Florida. When someone dies, inherited property receives a new cost basis equal to its fair market value on the date of death. This eliminates all capital gains that occurred during the decedent’s lifetime. Consider a concrete example: if someone purchased a home in Boca Raton for $200,000 but it appreciated to $600,000 by the time they died, the heir’s cost basis becomes $600,000. If the heir sells immediately at that price, there is no capital gains tax at all. This rule applies to stocks, mutual funds, real estate, and business interests. The stepped-up basis was preserved in the One Big Beautiful Bill Act, so this benefit remains available now. For families holding appreciated assets, understanding that inherited property receives this automatic tax reset is critical to planning decisions about whether to transfer assets during life or hold them until death.

Why Portability Requires Action

Portability sounds simple, but many surviving spouses miss the filing deadline and lose millions in tax savings. The surviving spouse must file IRS Form 706 within nine months of the first spouse’s death to elect portability. An extension can add six months, but the clock starts immediately.

Without this election, the first spouse’s unused exemption vanishes, and the surviving spouse can only use their own exemption when they die. For a married couple with a $30 million combined exemption, missing this deadline could result in a $4 million federal estate tax bill on the second death. The cost of filing Form 706 is minimal compared to the potential tax liability, yet many families overlook this requirement entirely.

Planning Ahead Protects Your Family’s Wealth

The combination of shrinking exemptions and the stepped-up basis rule creates both urgency and opportunity. High-net-worth residents in Palm Beach County should review their current plans now, not after 2026 when exemptions drop. Trusts, gifting strategies, and life insurance arrangements can all work together to minimize federal taxes. The next section covers the specific strategies that actually reduce your tax burden and protect your family’s inheritance.

How to Cut Your Federal Estate Tax in Half

Irrevocable Trusts Remove Assets From Your Taxable Estate

Trusts remain the most powerful tool for reducing federal estate taxes, but only the right structure works for your situation. A revocable living trust avoids probate and simplifies incapacity planning, yet it does nothing to reduce federal estate taxes because the IRS still treats you as the owner of all assets inside it. For estates likely to exceed the $15 million exemption threshold in 2026, irrevocable trusts actually remove assets from your taxable estate. An irrevocable life insurance trust (ILIT) keeps the death benefit outside your estate, potentially saving $400,000 in taxes on a $1 million policy for a high-net-worth Florida resident. A spousal lifetime access trust (SLAT) lets you gift $15 million to an irrevocable trust while maintaining access through your spouse, effectively doubling the tax-free wealth transfer for married couples.

Grantor Retained Annuity Trusts Transfer Appreciating Assets

Grantor retained annuity trusts (GRATs) have facilitated more than $100 billion in wealth transfers over the last decade according to the Federal Reserve, allowing you to transfer appreciating assets with minimal gift tax. The tradeoff is clear: irrevocable trusts require you to surrender control of assets permanently, but for families with substantial wealth, that loss of control is a small price for eliminating hundreds of thousands in federal taxes.

Annual Gifting Compounds Over Time

Annual gifting within the $19,000 per-recipient exclusion is the simplest tax reduction strategy available, and most high-net-worth residents ignore it entirely. You can gift $19,000 to each of your children, grandchildren, and other beneficiaries every single year without using any of your lifetime exemption. A married couple can gift $38,000 per recipient annually. Over ten years, a married couple with five adult children can transfer $1.9 million tax-free through annual gifts alone. The critical advantage is that any appreciation on those gifted assets occurs outside your estate, meaning future growth escapes taxation entirely.

Unlike inherited assets, lifetime gifts carry over your original cost basis, so beneficiaries may face capital gains taxes when they sell appreciated property. This means holding appreciated assets until death often produces better tax results through the stepped-up basis, but newer assets with modest appreciation benefit from lifetime gifting.

Portability Elections Require Immediate Action

Portability elections for married couples require filing IRS Form 706 within nine months of the first spouse’s death, yet countless families miss this deadline and forfeit millions in unused exemptions. The surviving spouse must file the form to elect portability; without this election, the first spouse’s unused exemption vanishes, and the surviving spouse can only use their own exemption when they die. For a married couple with a $30 million combined exemption, missing this deadline could result in a $4 million federal estate tax bill on the second death. The form costs less than $2,000 to prepare, but the potential tax savings exceed $4 million for couples with substantial combined assets. Filing the election takes minutes once the paperwork is complete, but failing to file it is permanent and irreversible.

The strategies above work best when coordinated with your overall financial and family situation. Each family’s circumstances differ, and the right combination of trusts, annual gifts, and portability planning depends on your asset levels, family structure, and long-term goals. Professional guidance helps you avoid conflicting strategies that can cost families hundreds of thousands in unnecessary taxes.

What Mistakes Cost Florida Families the Most Money

Outdated Plans Destroy Your Intentions

Stale estate plans silently kill wealth in Florida, and most residents never realize their documents are obsolete until far too late. Life changes like marriage, divorce, the birth of children or grandchildren, significant asset growth, or relocation to Florida should trigger an immediate estate plan review, yet the average person updates their plan only once every ten years, if at all. When a major life event occurs-remarriage, a child reaching adulthood, the purchase of investment property, or a substantial inheritance-your old plan no longer reflects your actual wishes. A will drafted when your children were minors may name guardians who have since moved away or passed. A trust created when your net worth was $1 million may lack strategies for the $5 million you’ve accumulated through business success or real estate appreciation.

The IRS reports that the federal exemption threshold will drop to $15 million per person starting January 1, 2026, which means families who had no tax concerns five years ago now face potential federal estate taxes unless they act immediately. Review your estate plan every two to three years at minimum, and immediately after any major life transition. This single practice prevents the vast majority of costly mistakes.

The Stepped-Up Basis Advantage Vanishes With Poor Decisions

The stepped-up basis rule is worth hundreds of thousands of dollars to Florida families, yet countless residents make permanent decisions that destroy this benefit without understanding what they’ve given up. When you inherit property, its cost basis resets to fair market value on the date of death, meaning all appreciation during the deceased’s lifetime vanishes for tax purposes. If your parent purchased a rental property for $300,000 and it’s worth $800,000 at death, you inherit it with an $800,000 basis-and you owe zero capital gains tax if you sell immediately at that price. Lifetime gifts destroy this advantage because they carry over the original cost basis, so transferring appreciated assets to children during life means they’ll owe capital gains taxes on the entire appreciation when they eventually sell.

The One Big Beautiful Bill Act preserved this benefit, but many families undermine it through poor planning decisions made years earlier. Holding appreciated assets until death often produces better tax results through the stepped-up basis than transferring them during life, especially for property that has appreciated significantly.

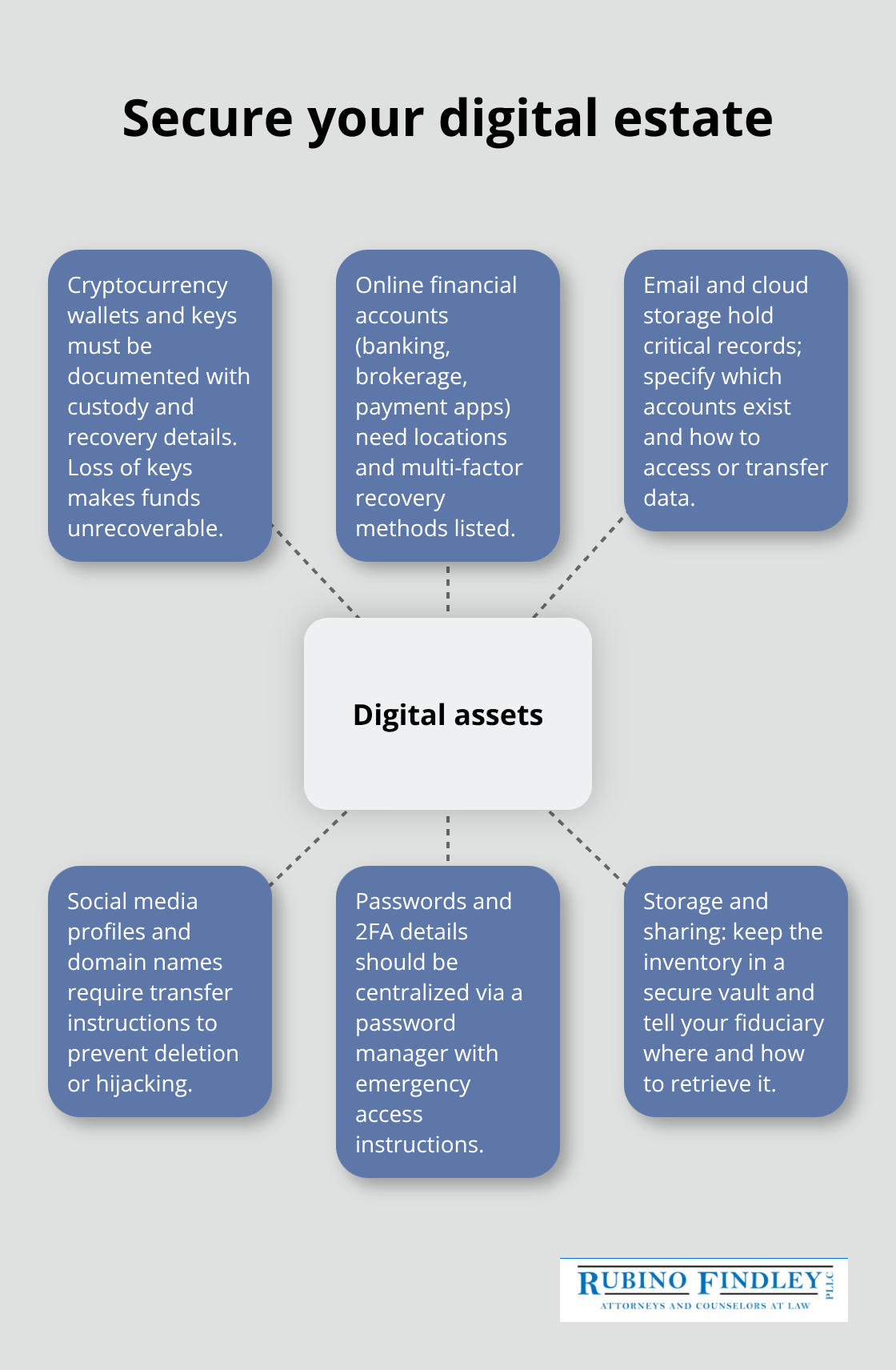

Digital Assets Disappear Without Explicit Instructions

Digital assets present an entirely different problem that most Florida residents ignore completely. The Federal Trade Commission reports approximately $2.7 billion in digital assets are lost annually due to insufficient planning, yet fewer than one in five people maintain a comprehensive digital asset inventory. Your digital assets include cryptocurrency holdings, online bank accounts, email accounts containing important documents, social media profiles, domain names, digital photos, and subscription services. Without explicit instructions about passwords, account locations, and transfer procedures, your heirs may never access these assets, and some digital accounts may be permanently deleted after months of inactivity.

Create a detailed inventory of every digital asset with usernames, recovery email addresses, and instructions for access. Store this inventory in a secure location and inform your trusted family members or attorney where to find it. These three mistakes-outdated plans, misunderstanding the stepped-up basis, and ignoring digital assets-account for the majority of lost wealth and family conflict in Florida estates, and all three are completely preventable with deliberate action.

Final Thoughts

Florida’s lack of state estate tax creates a significant advantage, but federal rules still apply to residents throughout Palm Beach County. This Florida estate taxes overview demonstrates that the stepped-up basis rule alone can save your heirs hundreds of thousands in capital gains taxes, while portability elections, annual gifting strategies, and irrevocable trusts work together to minimize federal taxes when you act with intention. The mistakes outlined above cost Florida families millions every year, and nearly all of them are preventable through deliberate planning and timely action.

Review your estate plan every two to three years, and take immediate action after major life changes such as marriage, the birth of children, significant asset growth, or relocation to Florida. Maintain a detailed inventory of your digital assets with clear instructions for access, and ensure your documents reflect your actual wishes rather than outdated intentions from years past. The cost of professional guidance is minimal compared to the potential tax savings and the peace of mind that comes from knowing your family is protected.

Contact Rubino Findley, PLLC to review your current plan and identify the strategies that work best for your circumstances in Palm Beach County. The time to act is now, before exemptions drop further and before life changes force reactive decisions instead of proactive planning.