Navigating Probate and Trust Administration

When a loved one passes away, families face complex legal processes that can feel overwhelming during an already difficult time.

Probate and trust administration involve different procedures, timelines, and requirements under Florida law. At Rubino Findley, PLLC, we guide families through these processes with clarity and compassion.

Understanding your options helps protect your family’s interests and honors your loved one’s wishes.

Key Differences Between Probate and Trust Administration

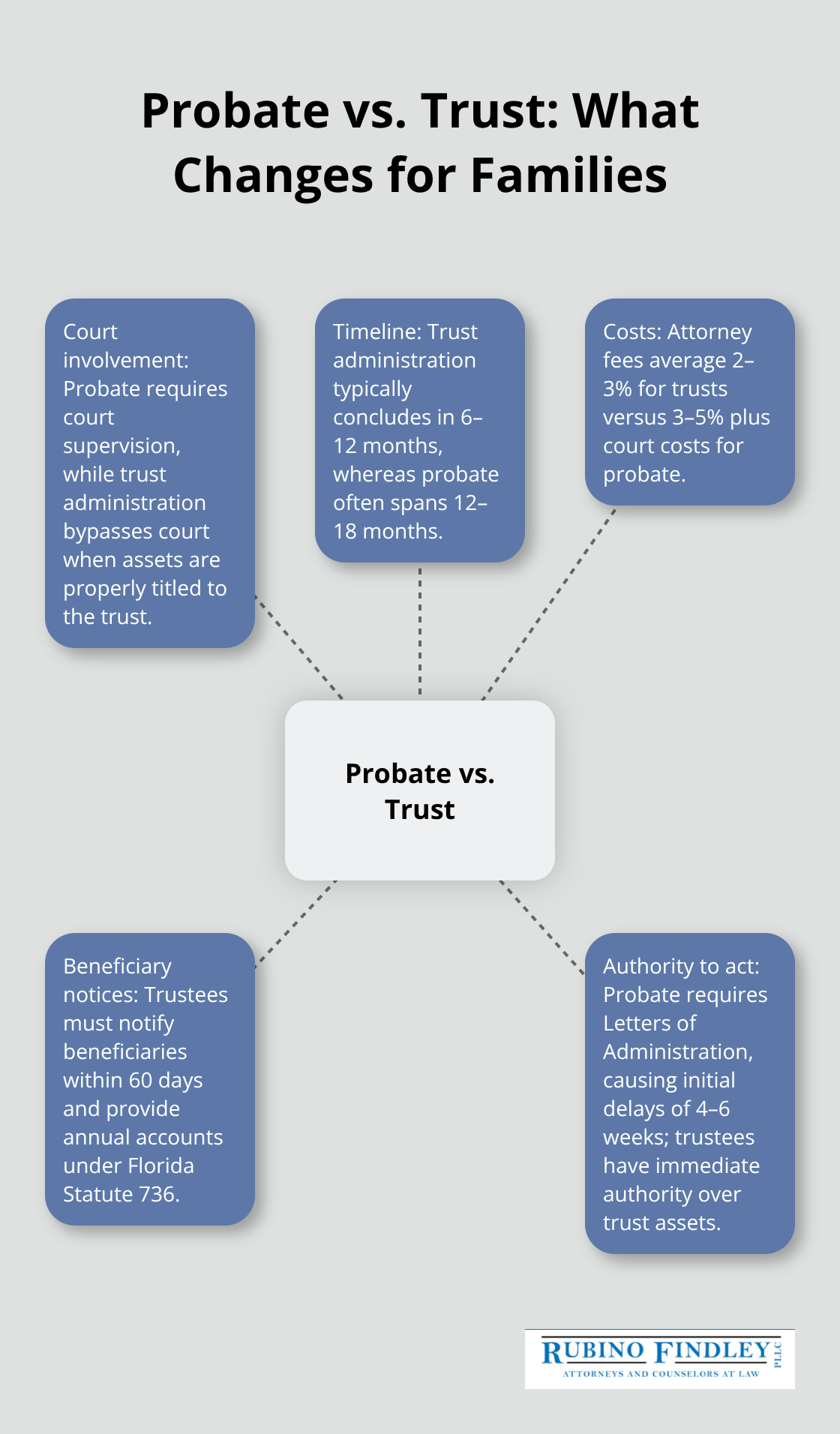

Probate administration takes place when someone dies with assets in their name alone, which requires court supervision to transfer ownership to beneficiaries. This process applies whether a will exists or not. In Florida, formal administration becomes mandatory for estates that exceed $75,000 or when the deceased passed away less than two years ago. Summary administration offers a faster alternative for estates under $75,000 or when more than two years have elapsed since death. The court must validate the will, appoint a personal representative, and oversee asset distribution according to Florida Statute 733.

Trust Administration Works Without Court Involvement

Trust administration bypasses court involvement entirely when assets carry proper titles in a trust’s name. The trustee manages and distributes assets according to the trust document without judicial oversight. Florida Statute 736 requires trustees to notify beneficiaries within 60 days of the settlor’s death and provide annual accounts. This process typically concludes within 6-12 months compared to probate’s 12-18 month timeline. Trust administration costs significantly less since attorney fees average 2-3% of asset value versus probate’s 3-5% plus court costs.

Florida Law Determines Your Timeline

Florida law mandates creditor notice periods that extend both processes. Probate requires newspaper publication and a three-month claims period, while trust administration involves direct creditor notification with a two-year statute of limitations (Florida Statute 95.11). The personal representative in probate must obtain Letters of Administration before access to any accounts becomes possible, which creates initial delays of 4-6 weeks. Trust administration begins immediately upon death since trustees already possess legal authority over trust assets.

Asset Transfer Methods Create Different Outcomes

Probate transfers assets through court orders after the judge validates the will and approves distributions. Trust administration transfers assets through trustee actions that follow the trust document’s specific instructions. Both processes face potential challenges, but the nature of these obstacles varies significantly between court-supervised and private administration methods.

Common Challenges in Probate and Trust Administration

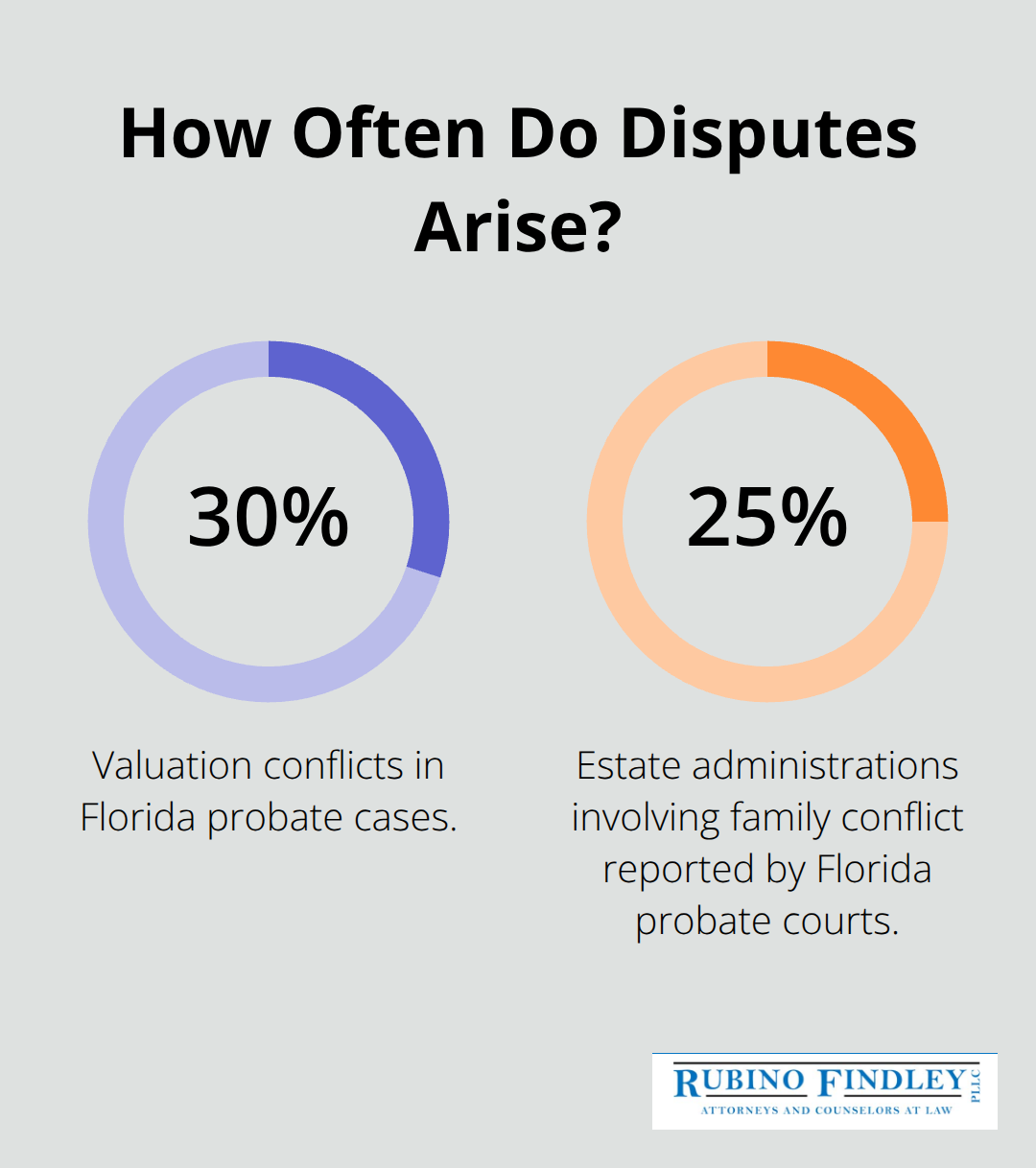

Asset disputes surface most frequently when families lack clear documentation about property values and intended distributions. Florida courts see valuation conflicts in approximately 30% of probate cases, particularly with family businesses, real estate, and collectibles. Personal representatives must obtain professional appraisals within 60 days of appointment, but beneficiaries often challenge these valuations when they believe assets deserve higher or lower assessments. Real estate appraisals prove especially contentious when market conditions shift between death and distribution dates. Multiple appraisals for high-value or unique assets help minimize disputes and provide courts with comprehensive valuation evidence.

Creditor Claims Create Complex Financial Webs

Florida’s creditor notification requirements generate substantial administrative burdens for both probate and trust administration. Probate estates must publish notices in local newspapers and directly notify known creditors, which creates a three-month claims period that extends the process significantly. Trust administration faces different challenges since creditors maintain a two-year window to file claims under Florida Statute 95.11. Medical debt, credit card balances, and tax obligations frequently exceed families’ expectations, with the average estate facing $15,000-$25,000 in outstanding debts according to Federal Reserve data. Personal representatives and trustees must verify each claim’s validity while they protect beneficiary interests, often through negotiations that delay final distributions for months beyond initial timelines.

Family Dynamics Intensify Under Legal Pressure

Beneficiary disagreements escalate when family members discover unequal distributions or unexpected provisions in wills and trusts. Florida probate courts report that 25% of estate administrations involve some form of family conflict, from minor disputes to full litigation. Spouses frequently clash with adult children over homestead property rights, while siblings dispute personal property distributions that lack specific documentation. Trust administration faces similar challenges when beneficiaries question trustee decisions about investment strategies or distribution schedules (Florida Statute 736.0813).

These conflicts multiply administrative costs and extend completion timelines by 6-18 months beyond normal periods.

Tax Obligations Compound Administrative Complexity

Estate and trust tax filings create additional layers of complexity that many families underestimate. Federal estate tax returns (Form 706) become mandatory for estates exceeding $12.92 million in 2023, but Florida imposes no state estate tax. Income tax obligations continue after death, requiring final personal returns and potential estate income tax filings. Trust administration involves ongoing tax responsibilities that trustees must manage throughout the distribution process. Professional tax guidance becomes essential when estates include business interests, retirement accounts, or complex investment portfolios that generate continued income after death.

These administrative challenges highlight why proper preparation and professional guidance prove invaluable when families face estate administration requirements.

Step-by-Step Guide to Probate and Trust Administration

Initial Court Filings Start the Process

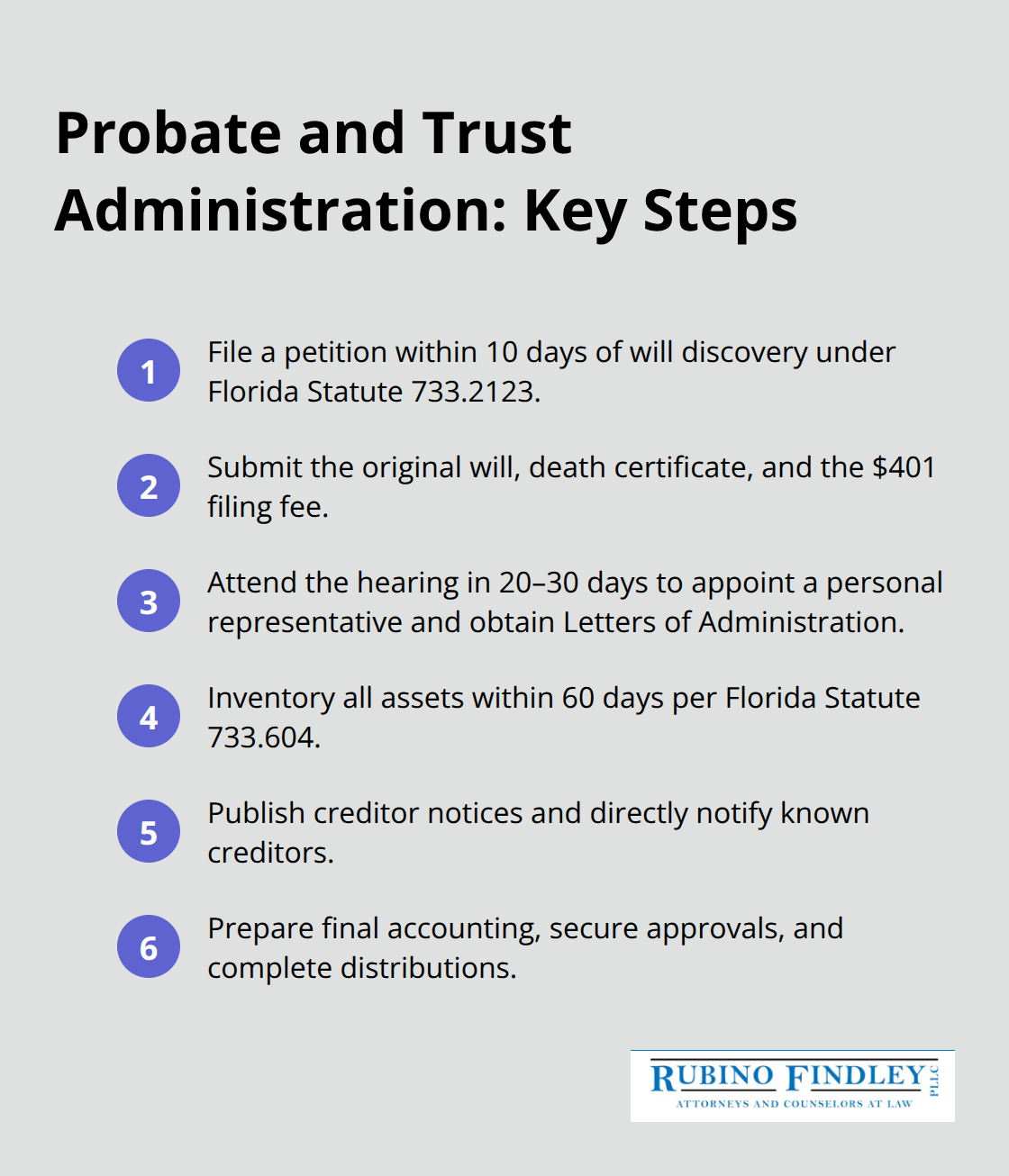

Probate administration begins when you file a petition in the deceased person’s county of residence within 10 days of will discovery under Florida Statute 733.2123. You must submit the original will, certified death certificate, and $401 filing fee to the clerk’s office. Florida requires formal administration for estates that exceed $75,000 or when death occurred within two years, while summary administration applies to smaller or older estates. The court schedules a hearing within 20-30 days to validate the will and appoint a personal representative who receives Letters of Administration. These letters grant legal authority to access bank accounts, sell property, and conduct estate business that banks and financial institutions require before they release any assets.

Asset Discovery Requires Systematic Investigation

Personal representatives must locate and inventory all estate assets within 60 days of appointment according to Florida Statute 733.604. This process involves contact with banks, investment firms, insurance companies, and employers to identify accounts, policies, and benefits. The Florida Department of Financial Services maintains an unclaimed property database that reveals forgotten accounts worth billions statewide. Professional appraisals become mandatory for real estate, business interests, and valuable personal property, with costs that typically range from $300-$800 per appraisal. Trust administration follows similar asset identification requirements, though trustees often possess better documentation since trust funding occurred during the settlor’s lifetime.

Creditor Claims Create Administrative Obligations

Both processes require detailed inventories that list every asset’s fair market value, which determines estate taxes and distribution calculations that affect final beneficiary payments. You must publish creditor notices in local newspapers for probate estates and directly notify known creditors (Florida Statute 733.2121). Trust administration faces different notification requirements since creditors maintain a two-year window to file claims under Florida Statute 95.11. Personal representatives must file detailed accountings, obtain court approval for major decisions, and follow strict notification procedures through negotiations that often delay distributions.

Final Distribution Follows Legal Protocols

Final distributions cannot occur until creditor claim periods expire and all debts receive payment through estate funds. Florida law requires a three-month creditor notice period for probate estates, while trust administration faces a two-year statute of limitations for unknown creditors. Personal representatives must file final accounting with the court that shows all income, expenses, and proposed distributions before they receive discharge orders. Trust administration concludes when trustees provide final accounting to beneficiaries and transfer assets according to trust terms. Both processes require tax clearances from the Internal Revenue Service and Florida Department of Revenue before final distributions occur, which can delay completion by 60-90 days beyond debt resolution.

Final Thoughts

Professional legal guidance transforms complex probate and trust administration from overwhelming burdens into manageable processes. Florida’s intricate statutes, creditor notification requirements, and court procedures demand thorough knowledge that protects families from costly mistakes and extended delays. We at Rubino Findley, PLLC help families navigate these challenging legal waters through comprehensive support that addresses every aspect of estate administration.

Our team handles initial court filings through final distributions while we keep families informed throughout each step. We understand that loss of a loved one creates emotional stress, which makes professional support invaluable during estate administration. Our approach addresses asset valuation disputes, creditor claims, and family conflicts before they escalate into expensive litigation (working with appraisers, tax professionals, and financial institutions to streamline processes).

Proper estate planning protects your family’s future and helps avoid probate complications entirely. We provide wills, trusts, and durable power of attorney services that secure your family’s financial interests. Contact Rubino Findley, PLLC for a free consultation to discuss your estate planning needs and learn how we can help protect your legacy.