Probate Accounting Requirements Florida: What Records You Must Keep

Administering an estate in Florida requires meticulous attention to detail, especially when it comes to probate accounting requirements. Poor record-keeping can delay the probate process, invite scrutiny from the court, and create unnecessary stress for your family.

At Rubino Findley, PLLC, we’ve seen how the right documentation practices protect estates and executors alike. This guide walks you through exactly which records matter and how to maintain them properly.

What Records Actually Get Tracked During Probate

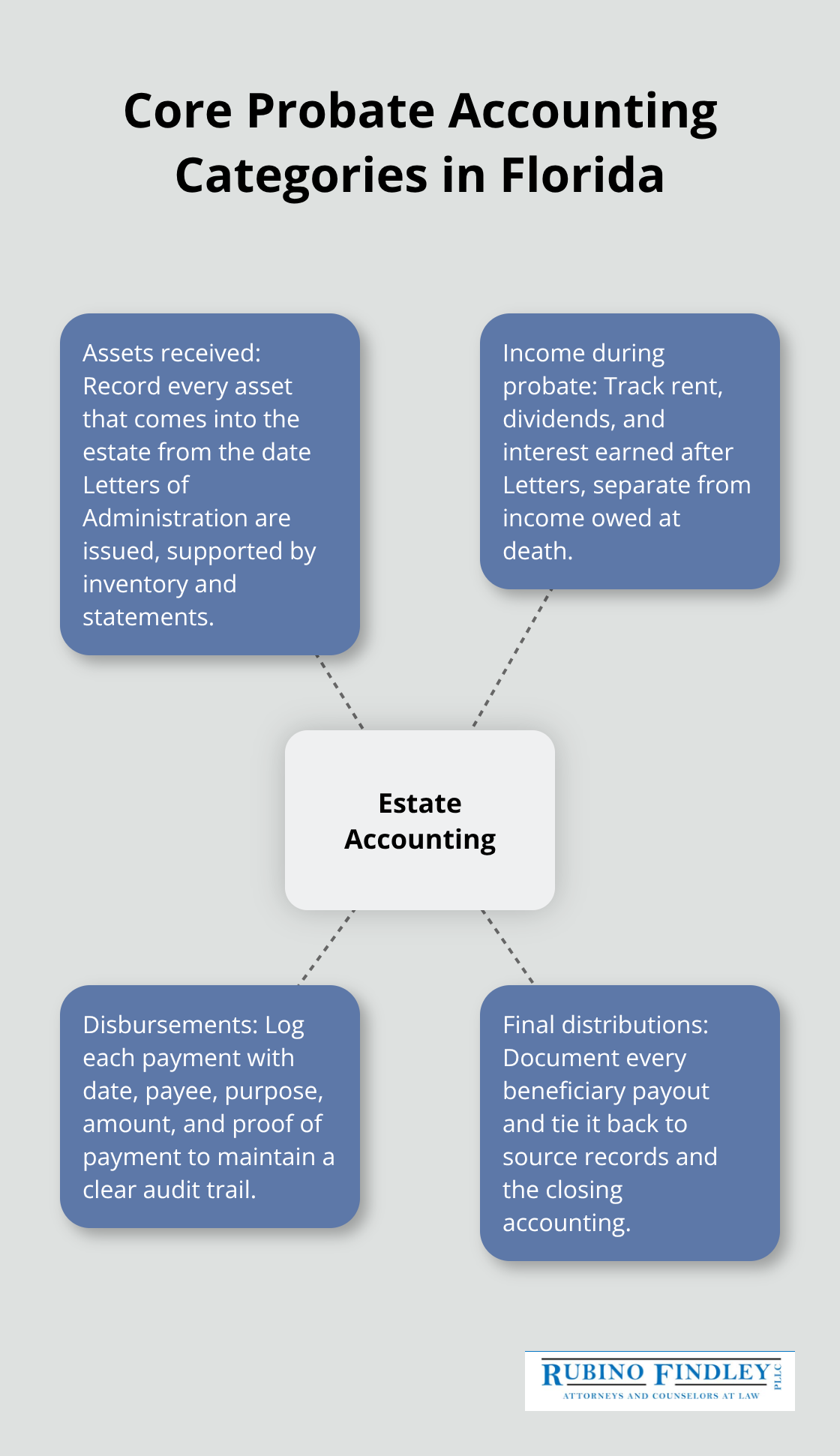

Probate accounting in Florida isn’t about guessing or approximating-it’s about documenting every single transaction from the moment the personal representative receives Letters of Administration until the estate closes. The personal representative must track four distinct categories: assets received, income earned during probate, all disbursements made, and final distributions to beneficiaries. This isn’t optional paperwork. Florida Statute 733.604 requires a verified inventory listing all estate property with its fair market value at the decedent’s death, filed with the clerk of the court.

If new assets surface later, an amended or supplementary inventory must be filed immediately. The court won’t approve closing an estate without a complete final accounting that ties every number back to source documents. Courts in Palm Beach County reject accountings that lack supporting documentation, forcing personal representatives to restart the filing process and delaying distributions by weeks or months.

Timing Creates Real Deadlines

The personal representative faces specific windows to meet. The inventory must be filed within a set timeframe after Letters issue. Income earned during probate gets separated from income owed at death-this distinction matters because it affects how much each beneficiary ultimately receives. The final accounting is due within twelve months after Letters if no federal estate tax return is required, or nine months after death if one is required, though extensions exist for complex estates. Missing these deadlines doesn’t just inconvenience the family; it signals to the court that the personal representative may not understand their obligations, inviting additional scrutiny of the accounting itself. Many probate cases stall because the personal representative waits too long to organize documents, then scrambles to reconstruct transactions months later when memories fade and records scatter. Starting documentation immediately, the day Letters arrive, prevents this entirely.

Documentation Standards Are Strict

The court expects traceable payment methods, not cash. Every expense needs a date, purpose, recipient name, and amount. Property taxes, homeowners insurance, maintenance costs, and professional fees all require receipts or invoices filed alongside the accounting. Fixed assets like vehicles, real estate, and jewelry must be revalued at the end of probate to ensure accuracy-the opening inventory value at death differs from the closing value, and the final accounting must show both.

If assets sell during probate, the proceeds must be tracked carefully and traced to how they were used. Beneficiary objections become likely when documentation is incomplete, especially for non-cash distributions of illiquid assets.

How Organization Affects Court Review

A personal representative who maintains detailed, organized records from day one faces far less court scrutiny and settles disputes faster than one playing catch-up months in. The next section covers the specific records you must maintain to satisfy these requirements and protect yourself from liability.

What Documents the Court Actually Demands in Boca Raton

The personal representative must maintain three categories of documents that the court will examine during the final accounting review. Bank statements showing every deposit and withdrawal form the backbone of probate accounting across Palm Beach County. Pull statements for the entire probate period from every account holding estate funds-checking, savings, money market, and investment accounts. Do not rely on online summaries; request official statements from each financial institution with transaction details. The court requires tracing every dollar from the moment the personal representative receives Letters of Administration.

Establishing Asset Values with Professional Documentation

If the estate holds real estate, vehicle titles, or jewelry, you need professional appraisals that establish fair market value at the decedent’s death, not current value. Florida Statute 733.604 mandates that the inventory list each asset with its estimated fair market value as of the death date. Courts reject inventories that estimate values without supporting appraisals for significant assets. Hire an appraiser within the first month after Letters issue; delays compound when you wait and property values shift.

Creating an Audit Trail for Every Expense

For expense documentation, the rule is absolute: no cash payments. Use checks, credit cards, or electronic transfers that create a paper trail. Every property tax bill, homeowners insurance premium, utility payment, and professional fee requires a receipt or invoice filed with the final accounting. Courts in Palm Beach County treat cash disbursements as red flags that invite creditor challenges and beneficiary objections. Create a spreadsheet on day one listing each expense category, the date paid, the amount, the vendor name, and the document reference. This prevents scrambling to locate receipts months later when the personal representative files the final accounting.

Tracking Asset Changes and Revaluations

Track revaluations of fixed assets at the end of probate separately from opening values. If a vehicle sold for $8,000 but was valued at $12,000 at death, both figures appear in the accounting with an explanation of the sale proceeds and how they were used. Beneficiaries often object when they see asset values drop during probate without understanding why; clear documentation of the reason (sale, market decline, or appraisal correction) stops disputes before they start. File an amendment to the inventory immediately if new assets surface after filing the original. Do not wait months to report discovered bank accounts or inherited property. The sooner you file the amended inventory under Florida Statute 733.604, the less likely the court questions your diligence.

Separating Income Sources to Prevent Disputes

Income earned during probate-rental income from real estate, dividend payments, or interest-must be separated from income owed at death in your records. This distinction directly affects how much each beneficiary receives. If the decedent owned rental property collecting $3,000 monthly, income received before death belongs to the decedent’s final return, while income received after probate administration opened belongs in the estate accounting. Maintain a simple log noting the income source, the date received, and whether it was owed at death or earned during administration. Beneficiaries who see income figures without this clarity often assume the personal representative mishandled funds or concealed amounts. Once you have these four document categories organized and filed, the next critical step involves understanding which common mistakes derail even well-intentioned personal representatives and how to avoid them entirely.

Where Personal Representatives Go Wrong in Boca Raton

The moment a personal representative receives Letters of Administration, a critical choice emerges: maintain separate accounts for estate funds or mix personal money with estate assets. Commingling personal and estate funds creates an immediate problem that courts in Palm Beach County treat as a serious red flag. When the personal representative deposits the decedent’s $50,000 into their own checking account alongside personal paychecks and household expenses, tracing which dollars belong to the estate becomes impossible. The court cannot approve a final accounting if it cannot verify that estate funds were used exclusively for estate purposes.

Separate Accounts Protect You From Liability

The personal representative then faces liability for any funds that appear to have been diverted, even if the money was genuinely used for legitimate estate expenses. Florida probate law demands an audit trail, not assumptions. Open a separate estate checking account at any bank within the first week after Letters issue. Name the account clearly: Estate of [Decedent Name], [Personal Representative Name], Personal Representative. This single step eliminates disputes and satisfies the court’s documentation requirements automatically.

Deposit all estate funds into this account and pay all estate expenses from it using checks or electronic transfers. Do not withdraw cash. Do not use a personal credit card to pay estate bills and reimburse yourself later. The court views these practices as sloppy at best and fraudulent at worst, and beneficiaries will challenge them aggressively.

Incomplete Documentation Invites Court Rejection

Incomplete documentation ranks as the second major failure point, and it stems from assuming the court will accept verbal explanations or general summaries. A personal representative who files an accounting stating that $15,000 was spent on estate administration without itemizing each professional fee, court filing, appraisal, or publication cost invites immediate rejection from the clerk’s office. The court needs the invoice from the appraiser, the receipt for the newspaper publication, the billing statement from the probate attorney, and proof of payment for each item.

Courts in Palm Beach County reject accountings that lack supporting documentation, forcing personal representatives to restart the filing process and delaying distributions by weeks or months. Each expense category requires its own documentation trail. Property taxes need the tax bill and proof of payment. Homeowners insurance requires the premium notice and receipt. Professional services require itemized invoices showing what work was performed and when. A spreadsheet listing expenses without attached receipts accomplishes nothing; the court will not approve the accounting.

Missing Deadlines Signals Loss of Control

Missing deadlines for required filings creates the third critical mistake, and this one costs real money in extended administration costs and beneficiary disputes. The inventory must file within the statutory window after Letters issue. If you discover new assets after filing the original inventory, file an amended inventory immediately rather than waiting to include them in the final accounting. Delays in filing amended inventories signal to the court that the personal representative lacks control over the estate, inviting heightened scrutiny of the final numbers.

The final accounting deadline varies depending on whether a federal estate tax return is required, but missing it means the court will not authorize distributions and the beneficiaries will not receive their inheritance. Professional guidance helps personal representatives navigate these phases without costly mistakes. Start documenting transactions on day one, not day 300. The sooner you establish systems for tracking assets, income, and expenses, the sooner you can file the final accounting and close the estate.

Final Thoughts

Probate accounting requirements in Florida demand precision and organization from the moment Letters of Administration arrive. The personal representative who maintains separate estate accounts, documents every transaction with receipts and invoices, tracks asset valuations carefully, and files amended inventories promptly avoids the delays and court rejections that plague disorganized estates. Starting documentation on day one rather than scrambling months later transforms probate from a stressful scramble into a manageable process.

Professional guidance matters because probate accounting in Florida involves statutory deadlines, confidentiality rules, and liability exposure that personal representatives often underestimate. A single missed deadline or incomplete filing can delay distributions by weeks or months and invite heightened court scrutiny. We at Rubino Findley, PLLC help clients navigate probate administration in Palm Beach County by handling the accounting requirements, coordinating with the court, and ensuring all documentation meets Florida standards.

If you are named as personal representative or facing probate administration, contact Rubino Findley, PLLC in Boca Raton for a consultation. We provide guidance on establishing proper record-keeping systems and meeting filing deadlines so your estate closes smoothly. Reach out today to learn how we can help protect you from liability.