Trust Administration Florida: Managing Your Trust With Confidence

Trust administration in Florida involves managing a deceased person’s assets according to their wishes. Many trustees face confusion about their legal obligations and deadlines, which can lead to costly mistakes.

We at Rubino Findley, PLLC serve Palm Beach County, Florida, and understand the complexities trustees encounter. This guide walks you through the process and shows when professional legal guidance makes a real difference.

What Trust Administration Actually Means

Understanding Your Role as Trustee

Trust administration in Florida is the legal process you use to manage and distribute trust assets after the grantor’s death or incapacity, governed by Florida Statutes Chapter 736. This isn’t theoretical-it’s a set of concrete, time-sensitive obligations that directly affect whether beneficiaries receive their inheritances on schedule and whether you avoid personal liability. Your primary job involves identifying, gathering, and managing all trust assets to preserve their value, paying valid debts and taxes before distributions, and communicating transparently with beneficiaries throughout the process.

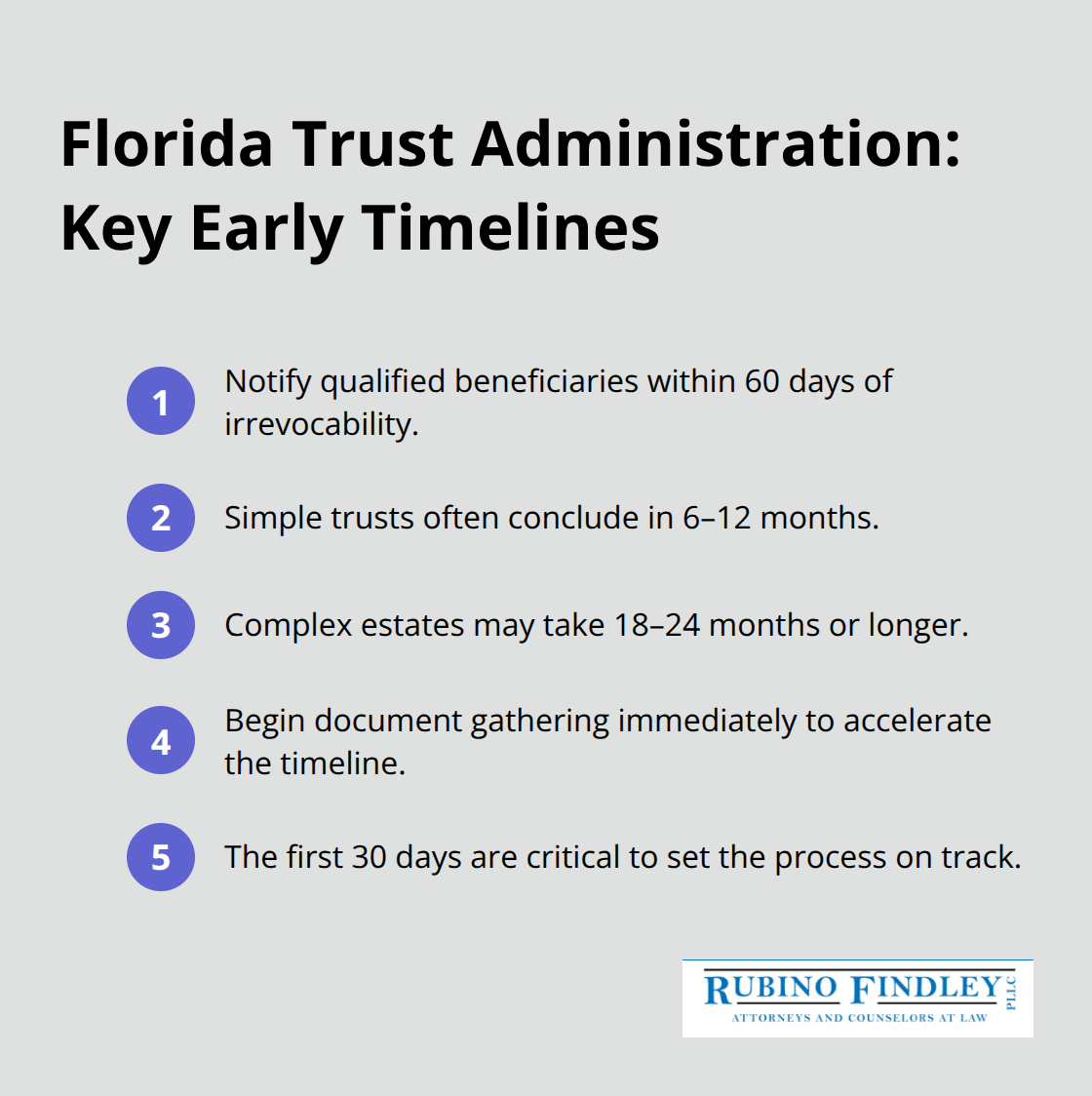

Florida law requires you to notify qualified beneficiaries within 60 days after a revocable trust becomes irrevocable due to the grantor’s death, per Florida Statute 736.0813. This notification must include your trustee details and beneficiaries’ right to a copy of the trust. The timeline matters significantly-simple trusts finish in 6 to 12 months, while complex estates can take 18 to 24 months or longer. Starting document gathering immediately can shave months off the timeline, which is why the first 30 days are critical.

Your First 30 Days: Critical Actions

During the initial month, you must locate and review the trust documents, obtain death certificates, secure assets, and start inventorying everything. This foundation determines whether the rest of the process runs smoothly or encounters delays. Many trustees underestimate how much work this phase requires, but rushing through it creates problems that compound later.

Fiduciary Duties That Carry Real Consequences

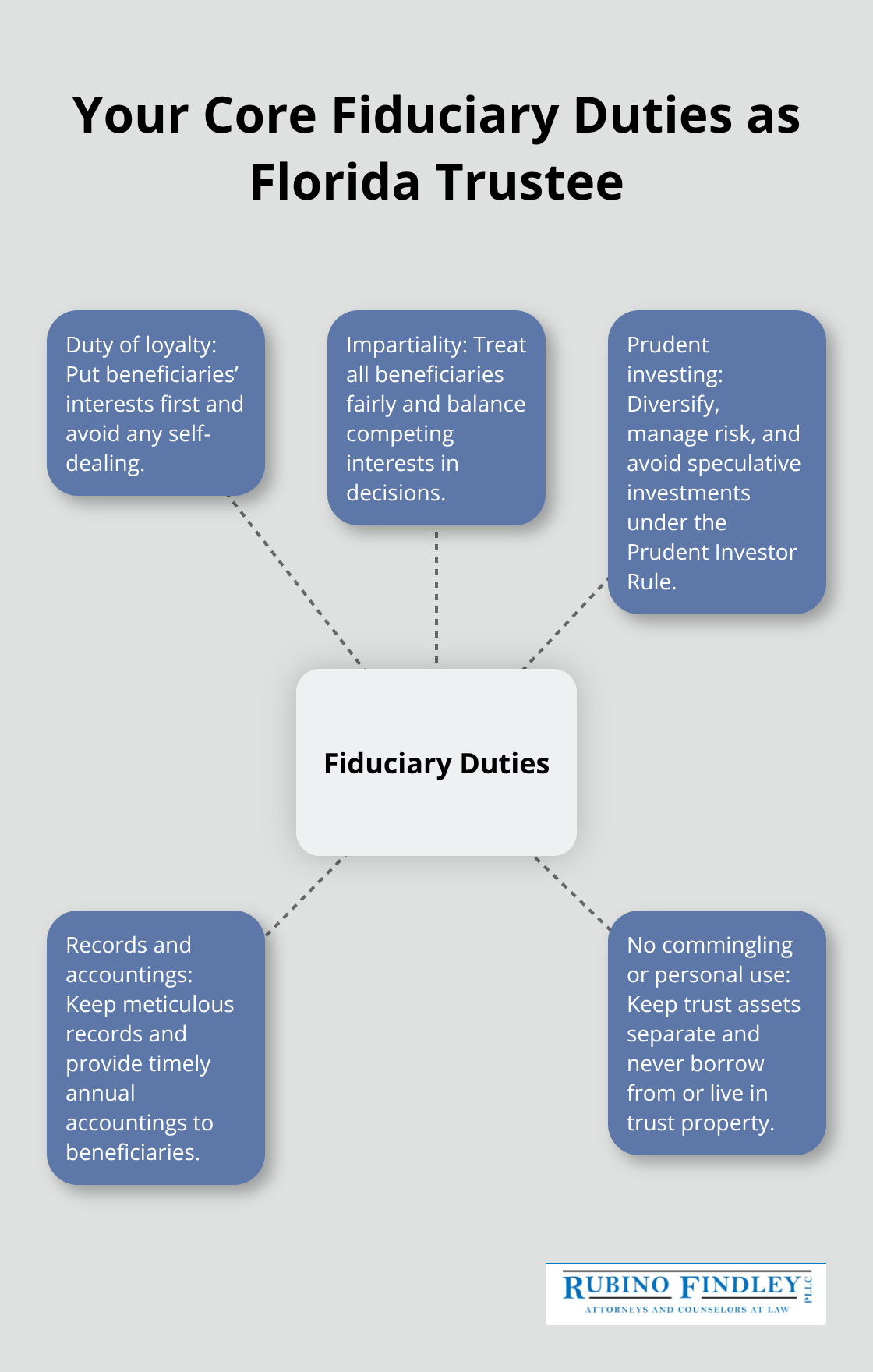

Your fiduciary duties under Florida law are non-negotiable and carry real consequences for violations. You must act in the best interests of beneficiaries at all times, avoiding conflicts of interest and self-dealing. Treating trust assets as personal property, taking personal loans from the trust, or living in trust-owned property for free can lead to your removal as trustee and personal liability. The duty of loyalty means you prioritize beneficiaries’ interests over your own, while impartiality requires treating all beneficiaries fairly when making decisions.

You also have a duty to invest prudently under the Prudent Investor Rule, diversifying assets, managing risk, and avoiding speculative investments. Florida law requires annual accountings to beneficiaries, so thorough recordkeeping prevents disputes and smooths deadlines. Many trustees make costly mistakes by rushing distributions, failing to maintain meticulous records, or commingling trust assets with personal accounts.

Protecting Yourself From Liability

Don’t rush distributions; waiting at least 6 months helps protect you from personal liability for unknown creditor claims. This waiting period gives you time to identify all valid debts and resolve title issues before making final payments to beneficiaries. Creditor claims typically have about 3 months from notice, but trust creditors can be exposed to a longer window (often cited as up to 2 years).

If you face complex issues like beneficiary disputes or significant tax planning questions, consulting with a trust administration attorney in Boca Raton who serves Palm Beach County, Florida is far less expensive than fixing mistakes later. The next section walks you through the specific steps Florida law requires during the administration process.

Moving Through the First Six Months

Organizing Your Assets in the First Month

The days immediately following the grantor’s death demand organized action. Within the first 30 days, you must locate and review all trust documents, obtain multiple copies of the death certificate, secure physical assets, and create a comprehensive inventory of everything the trust owns. This includes real estate deeds, vehicle titles, bank statements, investment records, retirement account details, insurance policies, loan documents, and personal property. Many trustees skip this step or rush through it, then spend months tracking down missing information.

Create a master spreadsheet listing all assets, account numbers, and contact information for financial institutions. This single document becomes your roadmap for the entire administration process and prevents costly oversights. The spreadsheet transforms a chaotic pile of paperwork into a manageable system that you can reference throughout the administration period.

Filing Notices and Establishing Trust Accounts

Between days 31 and 60, you must file a notice of trust with the court in the settlor’s domicile and notify all qualified beneficiaries per Florida Statute 736.05055. This notification must include your trustee details and beneficiaries’ right to a copy of the trust. Use certified mail or secure email with read receipts to prove delivery, since Florida law treats documentation as critical evidence. During months two through four, you establish trust bank accounts separate from your personal accounts, obtain a tax identification number for the trust, and have all assets professionally valued. This valuation date matters tremendously for tax purposes.

Commingling trust assets with personal accounts represents one of the most dangerous mistakes you can make. It exposes the trust to creditor claims against your personal finances and signals to beneficiaries that you are mismanaging their inheritance. Keep trust assets completely separate from the start.

Managing Debts and Timing Distributions Strategically

Months four through six involve filing necessary tax returns, resolving title issues on real estate, and reviewing valid debts. Many trustees want to distribute assets immediately, but this creates unnecessary risk. Creditor claims typically have about three months from notice, while trust creditors can pursue claims for up to two years. Waiting at least six months protects you from personal liability for unknown creditor claims and gives you time to address any liens or encumbrances on property.

During months six through twelve, you manage ongoing asset protection, provide the first annual accounting to beneficiaries, and address any beneficiary concerns. Florida law requires annual accountings with specific formatting requirements established since July 1, 2018. Beneficiaries can request detailed information within 30 days, and you have 30 days to provide requested documents. Prepare accountings that show income received, expenses paid, and distributions made-transparency here prevents disputes and demonstrates your competence.

Complying With Florida’s Notification and Title Requirements

Florida Statute 736.0813 requires you to notify qualified beneficiaries within 60 days after a revocable trust becomes irrevocable. This is not optional, and missing this deadline creates liability exposure. The Palm Beach County clerk must file and index the notice of trust like a caveat unless a probate proceeding exists. If the trust owns real property, you must ensure marketable title by addressing any title issues before distributing assets to beneficiaries.

Between months 12 and 24, you make final distributions after creditor claims are resolved, file final tax returns, and formally close the trust. Do not rush this phase-beneficiaries often challenge distributions made without proper accounting or tax resolution. A final accounting and court closure can provide you with a formal release from liability, which protects you from future claims. Document everything: create and preserve asset inventories, accounting records, receipts, and distribution histories. These records become your defense if disputes arise later.

As you move through these phases, complex situations often emerge that require professional guidance. The next section explains when hiring a trust administration attorney becomes essential to protect both the trust and yourself.

When to Hire a Trust Administration Attorney

Recognizing Complex Trust Situations

Trust administration costs escalate dramatically when mistakes accumulate, which is why knowing when to bring in legal help separates smooth administrations from painful ones. If the trust owns real estate in multiple states, includes business interests, or contains substantial investment portfolios, you need an attorney from the start. Out-of-state property creates title complications that require someone familiar with different jurisdictions’ requirements. A business interest means you must decide whether to sell, liquidate, or transfer ownership-each option carries different tax and liability implications. Large investment portfolios demand careful handling under Florida’s Prudent Investor Rule, which requires diversification, risk management, and documented decisions. If you are uncertain whether your trust fits this description, a single consultation with a trust administration attorney in Boca Raton who serves Palm Beach County, Florida typically costs $300 to $500 and takes one to two hours.

That conversation clarifies whether professional guidance throughout administration protects you from liability that could cost tens of thousands of dollars.

Handling Beneficiary Disputes Before They Escalate

Beneficiary disputes escalate quickly and destroy trust administrations that were otherwise proceeding smoothly. When beneficiaries disagree about asset valuations, interpretation of distribution terms, or your actions as trustee, the conflict becomes personal and legal simultaneously. Florida law gives beneficiaries 30 days to request detailed information about trust assets, and if you provide incomplete or unclear accountings, disputes multiply rapidly. If a beneficiary threatens to challenge your decisions or files a formal objection, you must stop distributions and consult an attorney immediately. Incomplete documentation signals mismanagement to beneficiaries and invites litigation that could have been prevented with transparent communication from the start.

Optimizing Tax Outcomes and Asset Protection

Tax planning decisions demand professional guidance because they affect both the trust and individual beneficiary tax returns. If the trust includes retirement accounts, life insurance policies, or significant income-producing assets, the tax strategy you choose determines how much beneficiaries ultimately receive. Failing to properly handle a grantor trust reimbursement or missing a deadline to disclaim inherited property can cost beneficiaries thousands in unnecessary taxes. The trust administration attorney you hire should coordinate directly with a tax professional to optimize outcomes and ensure compliance with federal and state requirements. These professionals work together to identify tax-saving opportunities that individual trustees often miss.

Protecting Yourself From Personal Liability

An attorney helps you document decisions, maintain proper records, and follow Florida Statutes Chapter 736 precisely. This protection matters most when disputes arise or when beneficiaries question your actions. A trust administration attorney in Boca Raton who serves Palm Beach County, Florida can review your accountings before you submit them to beneficiaries, catching errors that could trigger litigation. They also advise you on when to wait before distributing assets, how to handle creditor claims, and whether court approval is necessary for certain decisions. This guidance transforms administration from a stressful guessing game into a structured process with clear accountability.

Final Thoughts

Trust administration in Florida demands precision, documentation, and timely action from the moment the grantor passes away. Miss a deadline, fail to notify beneficiaries properly, or mishandle assets, and you face personal liability that can cost tens of thousands of dollars. The process requires you to balance competing demands-protecting assets, managing creditors, satisfying beneficiaries, and complying with Florida Statutes Chapter 736-while maintaining detailed records that prove your competence if disputes arise.

Most trustees benefit from professional guidance, especially during the critical first 60 days when notification deadlines loom and asset inventory decisions set the tone for the entire administration. Waiting at least six months before making final distributions, maintaining separate trust accounts, and documenting every decision protects you far more effectively than rushing through the process to satisfy impatient beneficiaries. The stakes are too high to navigate trust administration in Florida alone unless the trust is genuinely simple and all beneficiaries agree on every decision.

We at Rubino Findley, PLLC in Boca Raton serve Palm Beach County, Florida, and understand the real pressures trustees face. Contact Rubino Findley, PLLC to schedule a free consultation and clarify your next steps before costly mistakes take hold.